Emissions Linked Trading in the US and EU: A Comprehensive Overview

Emission-linked trading has emerged as a pivotal tool in the global fight against climate change. Both the United States and the European Union (EU) have made significant strides in developing comprehensive frameworks to regulate and facilitate emissions trading. This article will explore the intricacies of emissions-linked trading in these two regions, shedding light on key documentation platforms, the use of derivatives, and recent developments that underscore the growing importance of carbon markets in addressing climate challenges.

Documentation Platforms for Emission-Linked Trading

One of the critical aspects of emissions-linked trading is the documentation platforms that facilitate these transactions. In the United States and the EU, several platforms play a crucial role in ensuring the smooth functioning of carbon markets. Notable platforms include the International Swaps and Derivatives Association (ISDA), the International Emissions Trading Association (IETA), and the European Federation of Energy Traders (EFET).

Use of Derivatives in Carbon Markets

Derivatives are financial instruments that have gained significant traction in carbon markets. These instruments enable participants to manage risk and speculate on carbon credit prices. The most common types of carbon derivatives in over-the-counter (OTC) markets include forwards, options, and swaps.

Options, such as put and call options, provide buyers and sellers with the right, but not the obligation, to buy or sell carbon credits at predetermined prices on future dates. Put options allow the sale of credits, while call options enable the purchase of credits. Forwards, on the other hand, involve agreements to buy or sell carbon credits at a fixed price on a future date, with the buyer obligated to pay the agreed purchase price regardless of market conditions.

OTC Trading and Climate Exchanges

When engaging in carbon trading in the OTC markets, participants have three primary options for documentation platforms: ISDA, IETA, and EFET. These platforms serve as essential frameworks for structuring and executing emissions-linked transactions, providing clarity and legal certainty to market participants.

Furthermore, the development of climate exchanges has enhanced the carbon credit market by reducing credit risk through central counterparty arrangements and increasing liquidity. Europe, in particular, boasts a robust exchange-traded market with various exchanges offering standardized contracts.

Examples include the European Climate Exchange (ECX) in the UK, Powernext in France, and Nordpool in Germany. The ECX coordinates the marketing and sales of ECX Carbon Financial Instruments, which include futures and cash contracts for EU ETS allowances, further promoting transparency and liquidity.

Carbon Pools

Carbon pools have emerged as innovative spot trading platforms, primarily catering to small emitters allocated allowances under the EU ETS. These pools match buy and sell orders, promoting counterparty anonymity and increasing liquidity by grouping smaller orders into larger transactions.

Key Differences Between ISDA, IETA, and EFET Platforms

Each of these documentation platforms differs in terms of their approach to excess emissions penalties, force majeure clauses, settlement disruption, and failure-to-deliver provisions. Additionally, variations in payment and delivery dates, as well as options to opt out of physical settlement obligations, distinguish these platforms. Suspension events are also handled differently, highlighting the importance of understanding these distinctions when engaging in emissions-linked trading.

Recent Updates in Emissions Trading

In recent years, the global carbon market has experienced impressive growth, with the total value reaching a record €760 billion in 2021, marking a 164% increase. Factors contributing to this growth include the rise of voluntary initiatives, corporate demand for voluntary offsets, and the implementation of compliance carbon programs.

Revenues from carbon taxes and emissions trading systems (ETS) also saw a significant increase, reaching nearly USD 95 billion globally in 2022. These trends indicate a growing commitment to combatting climate change through emissions-linked trading mechanisms.

Kyoto Protocol vs. Paris Agreement

Emissions trading has evolved significantly since the Kyoto Protocol, which aimed to reduce emissions by 5% (2008-2012) and 18% (2013-2020) relative to 1990 levels. In contrast, the Paris Agreement sets more ambitious targets, striving to limit global warming to well below 2°C, with efforts to keep it below 1.5°C. The Paris Agreement embraces a bottom-up approach, relying on Nationally Determined Contributions (NDCs) to guide emissions reductions. This shift in approach emphasizes the importance of carbon pricing initiatives, including emissions trading, in achieving climate goals.

Carbon Pricing Initiatives

Carbon pricing initiatives play a vital role in emissions-linked trading. These initiatives determine the price per tonne of CO2 equivalent and include concepts like the social cost of carbon, the polluter pays principle, and internalization of climate externality. Policymakers must choose between taxation and market-based mechanisms, each with its advantages and disadvantages. While taxation offers lower transaction costs, market-based mechanisms provide more robust tools for achieving reduction targets.

Regulated Carbon Markets: EU ETS

The European Union Emissions Trading System (EU ETS) represents one of the world’s most prominent regulated carbon markets. Launched in 2005, the EU ETS covers over 10,000 installations, accounting for 45% of the European Union’s total greenhouse gas emissions.

The system employs a cap-and-trade approach, with a maximum threshold of emissions that decreases over time. Compliance entities trade allowances, and those falling short face fines. Over time, the EU ETS has undergone several phases, with changes to allocation methods and sector coverage to enhance environmental effectiveness.

Voluntary Carbon Markets

Voluntary carbon markets (VCMs) have gained prominence as businesses and individuals seek to offset their emissions voluntarily. These markets allow participants to acquire carbon credits to compensate for or offset their emissions. Carbon credits represent the reduction or removal of greenhouse gases from the atmosphere. VCMs offer a wide range of standards for verifying and validating projects, including the Verified Carbon Standard (Verra), the Gold Standard, and the Climate Action Reserve, among others.

Project Cycle and Registry

Projects within VCMs must adhere to specific cycles, including selecting a methodology, validation, verification, and issuance. Each step ensures that projects meet high-quality standards and deliver genuine emissions reductions. Registries track and record the issuance and transfer of carbon credits, promoting transparency and accountability in these markets.

Paris Agreement: Article 6

Article 6 of the Paris Agreement focuses on cooperation in the implementation of Nationally Determined Contributions (NDCs). It outlines mechanisms for internationally transferred mitigation outcomes (ITMOs) and the sustainable development mechanism (SDM). Corresponding adjustments ensure that emissions reductions are accurately accounted for and do not lead to double counting.

Recent Developments and Challenges

As voluntary carbon markets continue to grow, several trends and challenges have emerged. These include the definition and pursuit of “net zero” emissions, concerns related to greenwashing, the development of climate transition plans, and the need for sustainability disclosures. Increased scrutiny of VCMs, along with controversies surrounding carbon credits’ environmental benefits, underscores the importance of regulatory oversight and market integrity.

The CFTC’s Role in Voluntary Carbon Markets

The Commodity Futures Trading Commission (CFTC) in the United States has identified carbon trading as a top priority. The CFTC aims to play a more substantial role in regulating and overseeing voluntary carbon markets. It recognizes the need for regulatory oversight, fraud prevention, and enforcement to ensure the integrity of these markets.

Carbon as a Commodity

The CFTC views environmental carbon products as commodities within its jurisdiction. Given the rapid

growth of carbon markets, the CFTC is actively seeking to define its role in regulating these markets. This includes exploring oversight approaches similar to those applied to digital assets.

CFTC Carbon Trading Initiatives

The CFTC has taken several initiatives to address climate-related risks and promote transparency in carbon markets. These initiatives include the creation of the Climate Risk Unit and hosting events to gather stakeholder input. Additionally, the CFTC has established an Environmental Fraud Task Force to investigate fraud and misconduct in voluntary carbon markets.

Emissions-linked trading has become a pivotal tool in the fight against climate change, with both the United States and the European Union actively shaping the future of carbon markets. As these markets continue to evolve, regulatory frameworks, documentation platforms, and transparency will play crucial roles in ensuring their effectiveness.

The CFTC’s growing involvement underscores the significance of regulatory oversight in maintaining market integrity and addressing climate-related risks. As global commitments to emissions reductions grow, emissions-linked trading will remain a central mechanism in the transition to a sustainable, low-carbon future.

পাওয়ার অব এ্যাটর্নি মূলত এমন একটি দলিল যেটার মাধ্যমে একজন ব্যাক্তি অপর কোন ব্যাক্তিকে তার পক্ষআইনসঙ্গত কোন কার্যক্রম গ্রহণের অধিকার প্রদান করে থাকে। সাধারণত এ ধরনের কার্যক্রম গ্রহণের অধিকারলিখিত দলিলের মাধ্যমে দেওয়া হয়।পাওয়ার অব এ্যাটর্নি আইনের ২ ধারার (১)উপধারা অনুসারে পাওয়ার অবএ্যাটর্নি বলতে এমন কোন দলিলকে বুঝায় যেটার মাধ্যমে কোন ব্যাক্তি তার পক্ষে উক্ত দলিলে বর্ণিত কায-সম্পাদনের জন্য আইনানুগভাবে অন্য কোন ব্যাক্তি নিকট ক্ষমতা অর্পণ করেন বা করে থাকেন।

পাওয়ারঅবএ্যাটর্নিপ্রকারভেদ

সাধারণ দিক থেকে পাওয়ার অব অ্যাটর্নি দুই ভাগে ভাগ করা যেতে পারে যথা-

সাধারন পাওয়ার অব এ্যাটর্নি (General Power of Attorney)

বিশেষ পাওয়ার অব এ্যাটর্নি ( Special Power of Attorney)

সাধারনপাওয়ারঅবএ্যাটর্নি (General Power of Attorney)

সাধারন পাওয়ার অব এ্যাটর্নি সম্পর্কে সুনিদিষ্ট ভাবে পাওয়ার অব এ্যাটর্নি আইন ও বিধিমালায় আলোচনা করাহয়নি,

তবে আমরা এই ভাবে বলতে পারি যে–পাওয়ার অব এ্যাটর্নি আইনে ২(৭) ধারার অনুযায়ী

অপ্রত্যাহারয়োগ্য পাওয়ার অব এ্যাটর্নি চারটি (৪টি) ক্ষেএ রয়েছে ,

উক্ত ক্ষেএ ব্যাতীত স্থাবর বা অস্থাবর সম্পওি ছাড়াও যেকোন বিষয় সাধারন পাওয়ার অব এ্যাটর্নি দলিল সম্পাদন করা যায়।যেমন-স্থাবর সম্পওি ইজারা দেওয়ার ক্ষমতা অর্পণ,অস্থাবর সম্পওি বিক্রয় ক্ষমতা অর্পণ ইত্যাদি।

বিশেষপাওয়ারঅবএ্যাটর্নি ( Special Power of Attorney)

রেজিস্ট্রেশন আইনের ৩২ ধারার উদ্দেশ্য পূরণকল্পে একই আইনে ৩৩ ধারার অধিনে প্রস্ততকৃত পাওয়ার অবএ্যাটর্নি কে বিশেষ পাওয়ার অব এ্যাটর্নি বলে গন্য হবে। বিশেষ পাওয়ার অব এ্যাটর্নি দলিলকে খাস-মোক্তারনামানামেও সর্বাধিক পরিচিত।এখন কোন ব্যাক্তিকে যদি মোকাদ্দমা পরিচালনার জন্য ক্ষমতা দেওয়া হয়, তখন সেটাবিশেষ পাওয়ার অব এ্যাটর্নি অনুযায়ী করতে হবে;

পাওয়ারঅফএ্যাটর্নিশর্তগুলোকী

১) পাওয়ার অফ এ্যাটর্নি একটি নির্দিষ্ট মেয়াদ পর্যন্ত হতে হবে অবশ্যাই;

২) যদি পাওয়ার অব এ্যাটর্নি কোন জমি হলে অবশ্যাই দলিলটি রেজিস্ট্রেশন করতে হবে আইন অনুযায়ী;

৩) যে কারনে পাওয়ার অব এ্যাটর্নি করা হয়েছে তা স্পষ্টভাবে ব্যাখা করতে হবে;

৪) স্ট্যাম্প আইন অনুযায়ী তা স্ট্যাম্প করতে হবে এবং রিসিট গ্রহন করতে হবে;

৫) আবেদন অবশ্যাই রেজিস্টার্ড ব্যাক্তির কাছে

কোনকোনবিষয়েপাওয়ারঅফএ্যাটর্নিদলিলতৈরিকরাযাবেনা

ধারা ৪ অনুযায়ী এই বিষয়ে আলোচনা করা হয়েছে। তা হলেঃ

উইল সম্পাদন বা দাতা উইল নিবন্ধনের উদ্দেশ্য দাখিলকরন;

দত্তক গ্রহনের ক্ষমতাপত্র সম্পাদন বা দাতা দত্তক ক্ষমতাপত্র নিবন্ধনের উদ্দেশ্য দাখিলকরন;

দান বা হেবা সম্পর্কিত ঘোষনা সম্পাদান;

ট্রাস্ট দলিল সম্পাদন

সরকারীর দলিল বিশেষ বা সাধারন আদেশের মাধ্যেমে সম্পাদন;

দাতারবিরুদ্ধেযখনগ্রহীতাপ্রতারনাকরে

দাতার এখানে আইনী প্রতিকার হলো দন্ডবিধি অনুযায়ী ধারা ৪০৬ এবং ৪২০ অনুযায়ী মামলা দায়ের করতেপারবে জুডিশয়াল মেজিস্ট্রেট বা মেট্রেপলিটন ম্যজিস্ট্রট এর নিকট।

পাওয়ার অব এ্যাটর্নি প্রস্ততকরণে যা লাগবে তা নিম্নরুপঃ

১।মূল পাওয়ার অব এ্যাটর্নি দলিলপত্র ।

২। ব্যাক্তিদের রঙ্গিন ছবি দিতে হবে অবশ্যাই।

৩।ক্ষমতা প্রদানকারী ব্যাক্তি (Power Giver) এর বৈধ বাংলাদেশী জাতীয় । পরিচয়পত্র/পাসর্পোট/ডিজিটাল(১৭ডিজিট) জন্মনিবন্ধন সনদ কপি। তাছাড়া বিদেশী নাগরিক এর ক্ষেত্রে তার নিজ দেশের পাসপোর্ট ।

৪।ক্ষমতা গ্রহনকারী ব্যাক্তি(Power Receiver) বৈধ বাংলাদেশী জাতীয়

৫।ক্ষমতা প্রদানকারী ব্যাক্তি (Power Giver)এবং ক্ষমতা গ্রহনকারী ব্যাক্তি (Power Receiver) এর সদ্যতোলা ২কপি ছবি।(সাদা ব্যাক-গ্রাউন্ডযুক্ত)।

৬।ফি প্রদানের প্রমাণপত্র।

৭।ডাকে পাঠানোর ক্ষেএ অর্থ পরিশোধিত ও ঠিকানা লিখা ফেরত খাম।

একাধিক পাওয়ার অব এ্যাটর্নি গ্রহীতা নিয়োগ করা যাবে কিনা

পাওয়ার অব এাটর্নি একাধীক হবে কিনা তা পাওয়ার অব এাটর্নি আইনে সুনিদিষ্ঠ ভাবে উল্লেখ না থাকলেও ৯ধারায় একাধিক কথা উল্লেখ রয়েছে এই থাকে অনুমেয় যে-পাওয়ার অব এাটর্নি দলিল ক্ষে্েএ একাধিক পাওয়ারঅব এাটর্নি গ্রহীতা নিয়োগ করা যাবে, কিন্তু একাধিক গ্রহীতা নিয়োগ এ প্রধান উদ্দেশ্য থাকবে একজন কে মূখ্যএবং বাকিদের কে সহযোগী হিসাবে রাখা। প্রধান গ্রহীতার অনুপস্থিতে অন্যরা যাতে কাজ করতে পারেন।

পাওয়ারদাতাবিদেশেঅবস্থানকরলে

পাওয়ার অফ এটর্নি বিদেশ থাকা অবস্থায় ব্যক্তির দলিল বানানোর প্রক্রিয়া একটু জটিল।এই ক্ষেত্রে আইনটিসম্পর্কে সুস্পষ্টভাবে জানেন এমন কাউকে দিয়ে সঠিক ভাবে লিখে দূতাবাসের মাধ্যমে দলিলটি সম্পাদন ওপ্রত্যয়ন করে পাঠাতে হবে। যদি কোন ব্যক্তি দেশের বাইরে থেকে জমি বা সম্পত্তি বিক্রি করতে চায় তাহলেঅবশ্যাই তাকে রেজিস্ট্রেশন আইন এর ধারা ৩৩ অনুসরন করবেন। এখানে বলা হয়েছে পক্ষের নাম ও ঠিকানা, জাতীয় পরিচয় পত্র, রঙ্গিন ছবি দিতে হবে, গ্রহীতার ছবির উপর দাতা তা শনাক্ত করবেন , দূতাবাসে যাওয়া সিলনেওয়া, পররাষ্ট্র মন্ত্রালয়ে যাবে, ধারা ৮৯ অনুযায়ী রেজিস্ট্রেশন আইন অনুযায়ী, কালেক্টর এর নিকট পাঠাতেহবে। এবং স্ট্যাম্প করবেন এবং রেজিস্ট্রার অফিসে পাঠিয়ে দিবে এবং নং ১ বই জমা দিতে হবে। এই পর্যায়ে ওইদলিলের একটি ক্রমিক নম্বর ও তারিখ নির্দিষ্ট হবে। এই নম্বরটিই ওই পাওয়ার অব অ্যাটর্নি দলিলের নম্বর।তফশিল ক, ফর্ম ৩ অনুসরন করবে দলিল তৈরির সময়।

পাওয়ারঅবএ্যাটর্নিসম্পাদনেব্যক্তিগতউপস্থিতি

পাওয়ার অব এ্যাটর্নি সম্পাদনে ব্যক্তিগত উপস্থিতি ব্যক্তিগত উপস্থিতি বাধ্যতামূলক এবং আগমনের পূর্বে কবেযোগদান করবে সেটি নিচ্ছিত করতে হবে,,,তবে বিদেশে অবস্থান করে সেই ক্ষেত্রে ব্যাতিক্রম রয়েছে,উপস্থিতি বিষয়সিথিল করা হয়েছে।

এখন কেউ যদি ভার্চুয়াল পাওয়ার অব এ্যাটর্নি সম্পাদন করতে চাই সেটা সম্ভব নয় তবে, পাওয়ার অব এ্যাটর্নিদলিলপএ হাইকমিশনার এর কন্সুলার অফিসারের সম্মুখে স্বাক্ষর করতে হবে।

পাওয়ার অব এ্যাটর্নি কখন অবসান বা বাতিল হয়ে যাবে

কি কি কারনে পাওয়ার অব এ্যাটর্নি বাতিল হবে/হয়ে থাকে তা নিম্নরু্পঃ

১।নির্দিষ্ট মেয়াদের জন্য পাওয়ার অব এ্যাটর্নি করা হলে মেয়াদ শেষে বা উদ্দেশ্য সফল তা বাতিল বলে গণ্য হবে।যেমনঃ ১ জানুয়ারী ২০২৩ থেকে ১ জুলাই ২০২৩ পর্যন্ত হলে, সময় শেষ হলে বাতিল হয়ে যাবে;

২।পাওয়ার অব এ্যাটর্নি বাতিল বা প্রত্যাহার করা যায়। বাতিল করতে চাইলে যে অফিসে রেজিস্ট্রি করা হয়েছিল, সেই জেলার রেজিস্ট্রার বরাবর মোক্তারনামা বাতিলের লিখিত আবেদন করতে হবে।

৩। পাওয়ার অফ এ্যাটর্নি জারীকারী ব্যাক্তি দেওলিয়া, মারা গেলে, আইনী স্বত্বা বাতিল হলে সেই দলিল ও বাতিলহয়ে যাবে;

৪। যদি পাগল বা উন্মাদ হয়ে যায় তাহলে বাতিল হয়ে যাবে;

৫। যেখানে দলিলটি আইন অনুয়ায়ী নিবন্ধন করার প্রয়োজন ছিলো, সেক্ষত্রে করে নাই;

৬। যে ব্যাক্তির কাছে ক্ষমতা দেওয়া হয়েছে সে ব্যাক্তি যদি পাওয়াকারীর নিকট আবেদনের মাধ্যেমে যখন বাতিলহয়ে যায়;

৭যখন আইনী কোন পর্যায়ের মাধ্যেমে সমধানের মাধ্যেমে যখন বাতিল করা হয়, যেমনঃ বিরোধ হলেমধ্যেস্থতাকারীর মাধ্যেমে যখন কোন বাতিল সিদ্ধান্ত আসে।

৮সাধারণ পাওয়ার অব এ্যাটর্নি অবসানের ক্ষেত্রে দাতা ক্ষমতা গ্রহীতাকে ডাক রেজিস্টার্ডর মাধ্যমে ৩০ দিনেরনোটিশ দিয়ে প্রদত্ত ক্ষমতার অবসান ঘটাতে পারবেন। তা ছাড়া ক্ষমতা গ্রহীতাও একইভাবে মালিককে ৩০ দিনের নোটিশ সাপেক্ষে অ্যাটর্নির দায়িত্ব ত্যাগ করতে পারেন।

পাওয়ার অফ অ্যাটর্নি সংক্রান্ত আইনি সমস্যা ?

কোন প্রশ্ন বা আইনী সহায়তার জন্য, বাংলাদশের সেরা ল ফার্ম এর সাথে যোগাযোগ করুনঃ-ই-মেইল: info@trfirm.com ফোন: +8801847220062 +8801779127165, ঠিকানা– বাড়ি-810, রোড- 29 , Mohakhali DOHS, ঢাকা।

The Bangladesh Bank has authorized the institutions to maintain multiple types of foreign currency and convertible taka accounts. Bangladesh Bank’s rules for opening and maintaining these accounts.

Moreover, persons ordinarily residing in Bangladesh may establish and maintain ‘Resident Foreign Currency Deposit (RFCD)’ accounts in FC with foreign currency brought in upon their return from international travel. Detailed instructions for opening and administering these accounts are provided below.

Foreign Currency (FC) Accounts are available in the following foreign currencies:

Dollar (USD),

British Pound Sterling (GBP),

Euro, and

Japanese Yen.

Who can establish an FC account?

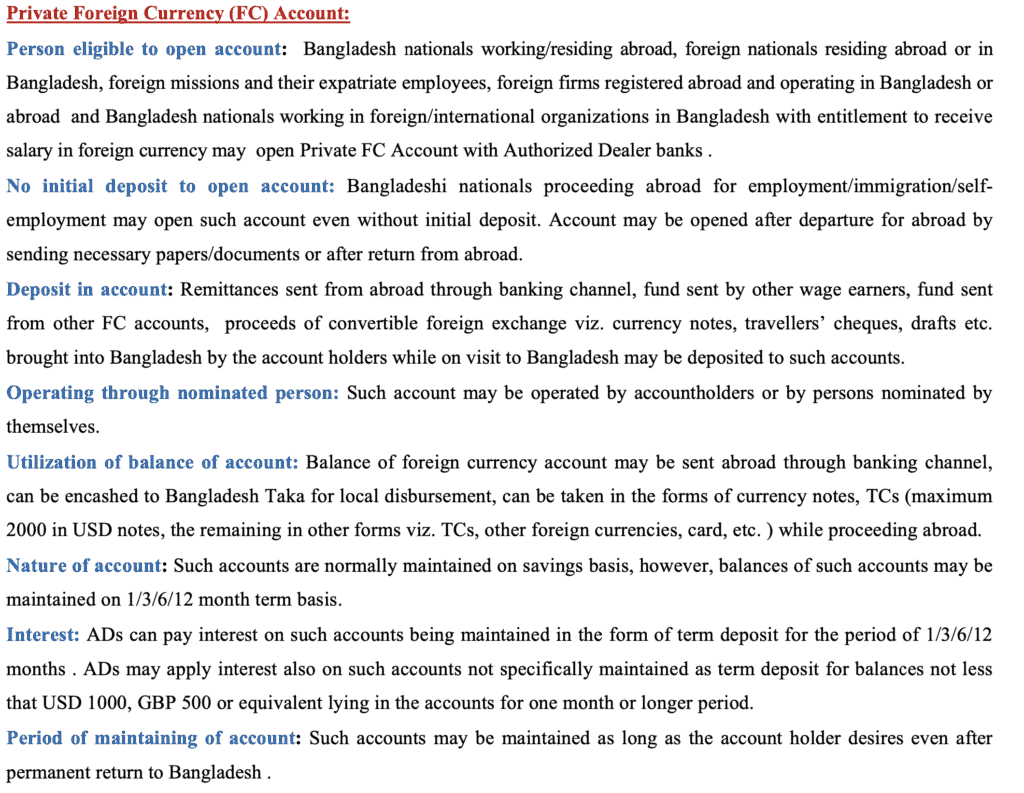

Bangladeshi nationals working or earning abroad, including self-employed Bangladeshi immigrants moving abroad for employment, are permitted to establish an FC Account without an initial deposit.

Foreign nationals residing abroad or in Bangladesh, as well as foreign firms registered abroad and operating abroad or in Bangladesh.

Missions abroad and their expatriate personnel.

Bangladeshi nationals employed by foreign or international organizations operating in Bangladesh, provided their salaries are paid in foreign currency or they receive consultancy fees or honoraria in foreign currency.

The customs authorities-licensed Diplomatic Bonded Warehouse (duty-free stores).

Local and Joint Venture contracting firms hired by foreign donors/international donor agencies to execute projects in accordance with the relevant contract, which will be closed as soon as the projects are completed.

Bangladeshi Shipping Firms and Airline Operators

Retention quota for merchandise exporters: Exporters providing inputs against back-to-back foreign currency letter of credit.

EPZ and EZ companies are permitted to establish foreign currency accounts.

Branch offices, liaison offices, and representative offices may establish FC accounts.

Note: A Private Limited Company operating outside of EZ/EPZ and registered under RJSC cannot establish an FC account.

Conditions, terms, and specifics of numerous FC account types:

Account in a Private Foreign Currency (FC):

Private FC Accounts can be opened at any of our Authorized Dealer locations.

Bangladeshi citizens living and working abroad;

b. foreign nationals residing in Bangladesh or abroad;

c. diplomatic missions and their expatriate personnel;

d. foreign firms registered overseas and functioning in Bangladesh or internationally;

e. Bangladeshi nationals employed by foreign or international organizations in Bangladesh who are eligible to be paid in foreign currency.

Accounts of the Diplomatic Bonded Warehouse for FC

ADs may establish foreign currency accounts in the names of Diplomatic Bonded Warehouses (duty-free shops) under the following conditions:

a. These accounts may only be credited with convertible foreign currency (notes and coins, travelers’ cheques, drafts, cheques or credit card settlements) received on account of the sale of merchandise.

b. Foreign exchange may only be transferred overseas for the import of goods by the bonded warehouse. Foreign exchange may also be transmitted from these accounts to foreign currency accounts maintained with other ADs for the same purpose.

Local and joint venture contracting enterprises’ FC accounts

– Individuals, including Bangladeshi nationals and non-resident Bangladeshis (NRBs) – Companies, corporations, and foreign investors.

Currency Options

FCAs can be maintained in various foreign currencies, such as USD, EUR, GBP, JPY, and more, subject to Bangladesh Bank’s approval.

Purpose of FCAs

– Facilitating international trade – Remittance of foreign earnings – Investment in Bangladesh – Holding foreign currencies for future use, and more.

Documentation

– For individuals: Valid passport, visa, and other KYC documents – For businesses: Incorporation documents, trade licenses, and more, depending on the type of account.

Opening Process

– Visit a bank authorized for FCAs with required documents – Fill out an account opening form – Choose the type of FCA – Deposit the required initial amount – Sign an account agreement

Operation of FCAs

– FCAs can be operated freely for authorized transactions. – Funds can be transferred abroad and back without significant restrictions.

Interest Rates

– The interest rates on FCAs vary and are typically lower compared to local currency accounts. Interest is paid based on the respective foreign currency.

Taxation

– Interest income from FCAs is generally tax-exempt in Bangladesh. – Capital gains tax may apply when converting foreign currency back to Bangladeshi Taka.

FC Accounts of Bangladeshi residents working for foreign/international organizations

Accounts in a foreign currency may be opened:

a. In the names of domiciled Bangladeshi nationals who are employed by foreign or international organizations operating in Bangladesh, if their salaries are paid in foreign currency.

b. This account may only be credited with the foreign currency portion of the salary and debited for all approved current transactions, such as travel expenses, the cost of children’s education, medical expenses, etc. These foreign currency accounts also allow for unrestricted local Taka withdrawals.

c. Consultancy fees/honoraria received in foreign currency by the aforementioned category of residents may also be credited to foreign currency accounts, with debits to such accounts subject to the same conditions as stated above.

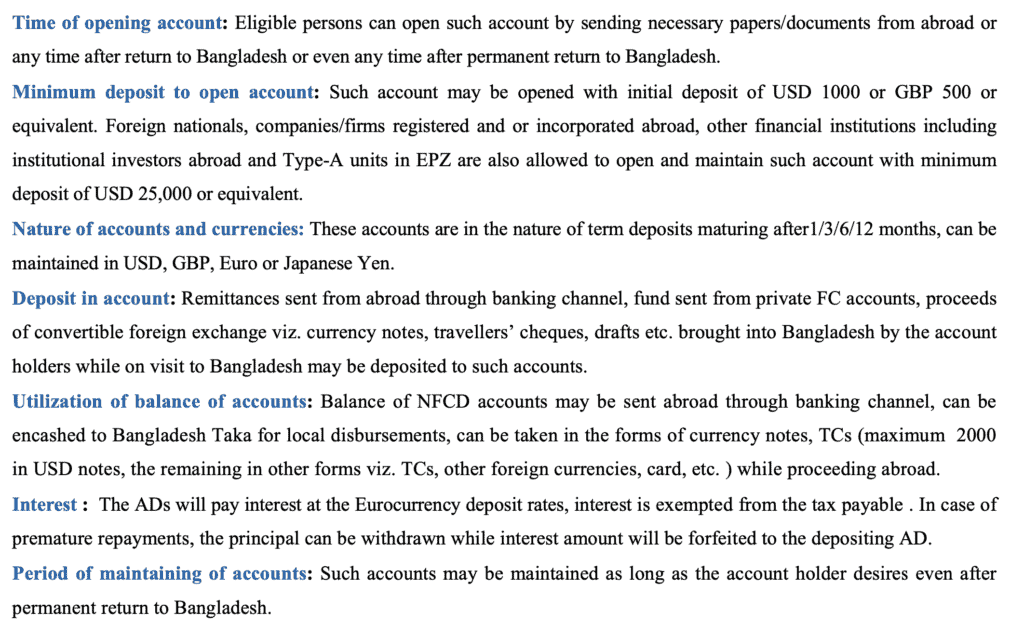

Account for Non-Resident Foreign Currency Deposits (NFCD):

NFCD accounts can be established at our Authorized Dealer locations by:

a. Bangladeshis living and working abroad

b. Bangladeshis with dual citizenship who reside abroad

c. Bangladeshi nationals operating abroad with Bangladeshi diplomatic missions

d. Officers/staff of the government/semi-government organizations/nationalized banks and corporate body employees posted abroad or deputed with international and regional agencies in foreign countries against foreign currency remitted through banking channels or carried in cash.

Account for resident foreign currency deposits (RFCD):

a. Individuals with a permanent residence in Bangladesh may establish an RFCD account with foreign currency brought back from a trip abroad.

b. Residents may establish this account at any time following their return to Bangladesh.

Account for Exporters’ Retention Quota (ERQ):

Retention quota accounts may also be established and maintained in the names of deemed exporters for supplying inputs against inland back-to-back foreign currency letter of credit.

ADs are required to strictly adhere to the following:

a. The total amount credited to the direct exporter’s retention quota account and foreign exchange paid to the presumed exporter for the supply of inputs cannot exceed the net repatriated amount.

b. FOB export value of the direct exporter; and The foreign exchange shall only be credited to the retention quota account of the deemed exporter upon resolution of the amount against back-to-back LC for deemed export.

Foreign currency accounts for enterprises in the EPZ:

The following procedures will govern the release of foreign currency to enterprises:

Exports originating from EPZs:

a. One hundred percent, eighty percent, and seventy-five percent, respectively, of repatriated export proceeds of Type A, B, and C and industrial unit in EPZ may be retained in FC account in the name of the unit with an AD in Bangladesh.

b. FC account balances may be freely used to satisfy all foreign payment obligations, including import payment obligations of the unit and foreign exchange payment obligations to BEPZA.

Individuals and businesses are able to establish FC accounts in Bangladesh based on their demand and requirements. Other FC accounts include Foreign currency accounts for Initial Public Offerings (IPO); Foreign currency accounts for shipbuilders (exporters); Foreign currency accounts of shipping companies, airlines, and freight forwarders; and Special FC accounts can be opened by obtaining BB’s permission and providing evidence.

Bangladesh Bank is the primary regulator of the country’s monetary and financial system, as well as the entity in charge of banking and financial legal services in Bangladesh. The Bangladesh Bank Order 1972- President’s Order No. 127 of 1972 (Amended in 2003) created it on December 16, 1971. The Governor is also the Chief Executive Officer of this historic institution.

The key tasks of the BB are:

• design and implementation of foreign currency policy; • holding and managing Bangladesh’s official foreign reserves; • authority for issuing Taka; and • monitoring banks and other financial institutions. •BB is governed by a number of laws, rules, and guidelines that help it carry out its responsibilities in regard to the economy’s monetary and fiscal systems. Some of these laws are as follows:

· Bangladesh Bank Order 1972; · Bank Company Act 1991 · Bank Company (Amendment) Act 2013 · Negotiatble Instrument Act 1881 · The Bankers’ Book Evidence Act 1891 · Foreign Exchange Regulations Act 1947 · Foreign Exchange Regulations (Amendment) Act 2015 · Financial Institutions Act 1993 · Financial Reporting Act 2015 · Money Loan Court Act 2003 · Money Laundering Prevention Act,2012 · Money Laundering Prevention (Amendment) Act, 2015 · Anti-terrorism Act, 2009

Mr. Tahmidur Rahman Remura Wahid, a law company in Bangladesh, offers clients confronting legal challenges in banking and finance both litigation and corporate services. Our banking and finance legal services in Bangladesh are provided by a team of experienced lawyers who prepare various documents required to obtain finance, review documents to be submitted to regulatory authorities, provide advice on obtaining finance, and resolve disputes both inside and outside of court using effective dispute resolution skills.

TRW has a significant banking and finance legal services clientele base in Bangladesh, both local and foreign, in the form of banks and other financial institutions, including but not limited to insurance companies, asset management organizations, and so on.

We often represent our clients in money suits, Negotiable Instruments Act 1881 cheque concerns, Money Loan Court Act 2003, Bank Companies Act 1991 mortgage disputes and redemptions, regulatory compliance and communications.

Tahmidur Rahman Remura Wahid, a Dhaka law firm, assists clients in arranging and or structuring loan transactions, project finance, trade finance, construction finance, mergers and acquisitions of corporate entities, resolving transactional disputes, conducting due diligence on mortgaged properties, and so on.

GLOBAL OFFICES: DHAKA: House 410, ROAD 29, Mohakhali DOHS DUBAI: Rolex Building, L-12 Sheikh Zayed Road LONDON: 1156, St Giles Avenue, 330 High Holborn, London, WC1V 7QH

Written by – Sourav Das, Junior Associate, TRW Law Firm

বাংলাদেশে তালাক সংক্রান্ত আবেদন, রেজিস্ট্রেশন,ফিস এবং পদ্ধতি এইসব বিষয়ে আলোচনা আছে কয়েকটিআইনে। সেগুলো আমি নিচে বিশদভাবে আলোচনা করবো। যেসব আইনে আমি আলোচনা আনবো তা হলোঃ

The Muslim Family Law Ordinance, 1961;

The Family Law Ordinance Act, 1985;

The Divorce Act, 1860;

The Dissolution of Muslim Marriage Act, 1939;

The Muslim Marriages and Divorces (Registration) Act, 1974’

The Muslim Family Law Ordinance, 1961 অনুযায়ী তালাকের বিষয়ে যা আলোচনা রয়েছেঃ

এই অধ্যাদেশের ধারা ৭ অনুযায়ী, তালাকের বিধানবলী আলোচনা করা হয়েছে। এখানে বলা হয়েছে যে, যদিকোন পুরুষ তার স্ত্রীকে তালাক ঘোষনার করে যেকোন পন্থা অবলম্বন করে। অতঃপর লিখিত ভাবে সেই তালাক নোটিশ ইউনিয়নের চেয়ারম্যানের এর কাছে এক কপি এবং স্ত্রী এর কাছে এক কপি সেন্ড করতে হয়। যদি তালাক বাতিলকরা না হয় প্রত্যেক্ষ বা পরোক্ষভাবে, তাহলে নোটিশ পাঠানোর ৯০ দিনের মধ্যে তালাক কার্যকর হবে নাহ।

নোটিশপাওয়ারপরচেয়ারম্যানএরদায়িত্ব

ধারা ৭ অনুযায়ী চেয়ারম্যান নোটিশ পাওয়ার পর, ৩০ দিনের মধ্যে চেয়ারম্যান দুইপক্ষের মধ্যে সালিশি এবং পুনর্মিলন এর জন্য সালিশি কাউন্সিল গঠন করবেন। সালিশি কাউন্সিল গঠনের মাধ্যেমে সকল রকমের পদক্ষেপনেওয়ার মাধ্যেমে পুনর্মিলন এর সব ধরনের ব্যবস্থা গ্রহন করবেন।

গর্ভাবস্থায়তালাকএরনিয়ম

যদি তালাক ঘোষনা দেওয়া অবস্থায় কোন স্ত্রী গর্ভাবস্থায় থাকে, যতদিন এর সময় থাকে অথবা ৯০ দিন যেটাআগে শেষ হয়।

তালাক দেওয়ার ছাড়া অন্য ভাবে তালাক এর পদ্ধতি

ধারা৮ অনুযায়ী বলা হয়েছে যে, তালাক দেওয়ার অধিকার যখন স্ত্রী এর উপর অর্পণ করা হয়েছে বা, দুই পক্ষআলোচনা সাপেক্ষে তালাক দেওয়ার জন্য সম্মতি প্রদান করেছেন সেই ক্ষেত্রে ধারা৭ প্রযোজ্য হবে।

The family Law Ordinance, 1985 অনুযায়ীতালাকদেওয়ারপদ্ধতি

১। এই অধ্যাদেশ এর অধীনে কোন ব্যক্তি যদি তালাক চায় তাহলে তাকে অবশ্যাই সহকারী জজ এর আরজি দাখিলের মাধ্যেমে তালাক গ্রহন করতে হবে তা করতে হবে ৩০ দিনের মধ্যে। আরজিতে ঠিকানা, কারন, ফিস, কাগজপত্র এইসব বিষয় উল্লেখ থাকবে এবং শুনানীর সময় কোন দস্তাবেজ যদি আদালতে পেশকরতে চায় তাহলে সেক্ষেত্রে অবশ্যাই আদালতের অনুমতি নিতে হবে।

২। আরজি দাখিলের পর সুমন প্রেরনের মাধ্যেমে ৩০ দিনের মধ্যে লিখিত জবাব দিতে হবে আদালতে সাথেপ্রাসঙ্গিক দস্তাবেশ এর মাধ্যেমে, এই সময়ের মধ্যে দাখিল করতে না পারলে আদালত ২১ দিনের বেশি নয়এমন সময় দিতে পারবে।

৩। যদি নির্ধারিত শুনানীর সময় কোন পক্ষ আদালতে উপস্থিত হতে ব্যর্থ হয় তাহলে আদালত মোকাদ্দমা টিখারিজ করে দিতে পারে এবং সেই খারিজ এর বিপরীতে দেওয়ানী কার্যবিধির আদেশ ৯, বিধি ৯ অনুযায়ীআবেদন দায়ের করতে পারে। যদি বিবাদী উপস্থিত না হয় তাহলে, বিবাদীর বিরুদ্ধে এক তরফা আদেশজারি হবে এবং বিবাদী উপযুক্ত কারন দেখালে তাকে আরো ২১ দিনে সময় দিবে আদালত।

৪। আদালত এই পর্যায়ে এসে মধ্যস্থতার কথা বলতে পারে যা আইনের ১০(৩), এবং ১৩(২) অনুযায়ী বলাহয়েছে।

৫। যদি মধ্যস্থতা করতে ব্যর্থ হয় পক্ষ তাহলে আদালত শুনানী এবং পক্ষের বক্তব্য শুনে রায় বা আদেশ দিতেপারে।

তালাক এর জন্য ফিস

ধারা ২২ এ বলা হয়েছে যে, যখন পারিবারিক আদালতে মোকাদ্দমা দায়ে করা হবে আদালত ফিস দিতে হবে ২৫টাকা।

আপিলকরারবিধান

পারিবারিক আদালতের এর রায়, আদেশ বা ডিক্রির বিরুদ্ধে ৩০ দিনের মধ্যে জেলা আদালতে আপিল দায়েরকরতে হবে। জেলা আদালতের আপিল চাইলে অতিরিক্ত জেলা আদালতের কাছে পাঠাতে পারে সিদ্ধান্ত, রায় বাআদেশ দেওয়ার

জন্য।

পারিবারিকআদালতেরায়হওয়ারপরকার্যক্রম

ধারা ২৩ অনুযায়ী বলা হয়েছে যে, আদালত এই অধ্যাদেশ এর বিধি মেনে রায় বা আদেশ দিয়ে সেখানেঅবশ্যাই, সে ডিক্রি সালিশি কাউন্সিল এর কাছে ৭ দিনের মধ্যে পাঠাবে রিসিপ্ট সহ এবং চেয়ারম্যান এমনভাবেপদক্ষেপ নিবে, যা তার কাছে তালাক হিসেবে এসেছে। চেয়ারম্যান ডিক্রি রিসিপ্ট পাওয়ার ৯০ দিনের পূর্ব পর্যন্ততালাক কার্যকারিতা হবে নাহ।

The Divorce Act, 1860 অনুযায়ীতালাকপ্রদানেরনিয়ম

এই আইনের ধারা ১০ অনুযায়ী, পুরুষ এবং স্ত্রী উভয়পক্ষ পিটিশন দায়ের করার মাধ্যেমে তালাক চাইতে পারে। পুরুষ ব্যভিচারের এর ভিত্তিতে জেলা আদালত বা উচ্চ আদালতে পিটিশন দায়ের করতে পারে। স্ত্রী তালারপিটিশন দায়ের করার কিছু ভিত্তি প্রয়োজনীয়ঃ

ব্যভিচার করে

ব্যভিচার করার মাধ্যেমে অন্য মহিলার সাথে বিবাহ আবদ্ধ হয়;

ধর্ষণ, যৌনতা পাশবিকতা;

যদি শুনানী করে আদালত মনে করে কোন যে, কোন রকম ব্যভিচারে এর প্রমান পাওয়া যায় নি, তাহলে আদালতপিটিশন টি খারিজ করে দিবে। খারিজ করলে সেই আদালতে রেভিউ এবং উচ্চ আদালতে রিভিশন দায়ের এরঅধিকার থেকে বঞ্চিত হবেন না। প্রমান পেলে উচ্চ আদালতের বিভাগ এর অনুমতি ব্যাতিত কোন আদেশ বারায় বা ডিক্রি প্রদান করিবেন না।

যদি খারিজ উচ্চ আদালত বিভাগ করে, তাহলে এর বিপরীতে কোন নতুন পিটিশন দায়ের করা যাবে নাহ। উচ্চআদালত কোন নিসি ডিক্রি দিলে তা ৬ মাস শেষ না হওয়া পর্যন্ত কার্যকর হবে নাহ।

The Dissolution of Muslim Marriages Act, 1939 অনুযায়ীতালাকপ্রদানেরনিয়ম

যদি বিনা কারনে ৩ বছর যাবত প্রাসঙ্গিক চাহিদা পূরন করতে ব্যর্থ হয়;

যদি স্বামী বিয়ের সময় থেকে পুরুষত্বহীন থাকে এবং চলতেই থাকে;

যদি স্বামী ২ বছর ধরে পাগল বা উন্মাদ অবস্থায় থাকে;

মহিলার অভিবাবক বা অন্য অভিবাবক ১৮ বছরের পূর্বে জোরপূর্বক বিয়ে দেয়;

স্বামী অমানবিক আচরন করে এবং শারীরিক ও মানসিক নির্যাতন করে;

মহিলার অনুমতি ছাড়া সম্পত্তি নিষ্পত্তি করা এবং তাকে কোন আইনী অধিকার চর্চা করতে বাধা প্রদান;

যদি এক বা একাধিক স্ত্রী থাকে মুসলিম আইন অনুযায়ী সমান ভাবে তার সাথে আচরন করে নাহ;

অন্য কোন আইন ধারা বিধিবদ্ধ বিবাহ বিচ্ছেদ এর কোন কারন;

কোন ডিক্রি স্বামীকে নোটিশ না দিয়ে করা যাবে নাহ, যদি তিনি নিখোজ থাকে তাহলে তার বৈধ প্রতিনিধির কাছেনোটিশ জারি হবে

২ধারারঅধীনডিক্রিকখনবাতিলকরাহয়

ডিক্রি ৬ মাস অতিক্রম না করা পর্যন্ত কার্যকর হিসেবে গন্য করা হবে নাহ, এই সময়ে যদি স্বামী আদালতে উপস্থিতহয়ে জবানবন্দি দেয় যে, তিনি সকল ধরনের চাহিদা এবং দায়িত্ব পালন করবেন, তাহলে আদালত ডিক্রি খারিজকরে দিবে।

The Muslim Marriages and Divorces Registration Act, 1974 এরআইনঅনুযায়ীবিবাহবিচ্ছেদনিবন্ধনএরপ্রক্রিয়া

এই আইনের ধারা ৬ এ বলা হয়েছে যে, বিবাহ বিচ্ছদ এর নিবন্ধন এর জন্য মৌখিকভাবে আবেদন দাখিলেরমাধ্যেমে করতে হবে বিবাহ নিবন্ধক এর কাছে। যদি বিবাহ নিবন্ধক আবেদন গ্রহন না করলে, ৩০ দিনের মধ্যেআবেদন কারী রেজিস্ট্রার এর নিকট বিবাহ নিবন্ধন এর জন্য আবেদন করবেন, অগ্রাহ্য নিবন্ধন এর কপি সহ।

যেসবকাগজপত্রবিবাহবিচ্ছেদএরসময়প্রয়োজনীয়

বিবাহ নিবন্ধন এর কপি;

জাতীয় পরিচয় পত্র এর রঙ্গিন কপি;

যদি কোন বৈধ কারনের প্রমান থাকে;

স্বামী সাজাপ্রাপ্ত থাকলে বা অসুস্থ থাকলে সেই কারনে বিচ্ছেদ এর প্রমাণস্বরূপ;

আইনের নাম

তালাক প্রদানের পদ্ধতি

The Muslim Family Law Ordinance, 1961

– পুরুষ যদি স্ত্রীকে তালাক ঘোষনা করে, তাকে লিখিত নোটিশ ইউনিয়নের চেয়ারম্যানের কাছে এবং স্ত্রীকে দেওয়া হয়। 90 দিনের মধ্যে তালাক কার্যকর হবে না। – চেয়ারম্যান নোটিশ পেলে 30 দিনের মধ্যে সালিশি এবং পুনর্মিলনের জন্য সালিশি কাউন্সিল গঠন করবেন।

The Family Law Ordinance Act, 1985

– তালাক চাইলে অবশ্যই সহকারী জজের আরজি দাখিল করতে হবে, তা হলো 30 দিনের মধ্যে। – আরজিতে ঠিকানা, কারন, ফিস, কাগজপত্র এইসব বিষয় উল্লেখ থাকবে।

The Divorce Act, 1860

– পুরুষ এবং স্ত্রী উভয়পক্ষ পিটিশন দায়ের করে তালাক চাইতে পারে। – স্ত্রীর পিটিশনে কিছু ভিত্তি প্রয়োজন, যেমন ব্যভিচার, ধর্ষণ, যৌনতা পাশবিকতা, ইত্যাদি। – তালাক নিয়ে প্রাসঙ্গিক দলিল হলে আদালত তালাক দেওয়া বাতিল করতে পারে।

The Dissolution of Muslim Marriage Act, 1939

– মহিলা বিবাহ বিচ্ছেদ এর ডিক্রি অর্জন করতে পারে, তবে কিছু শর্ত আছে, যেমন ব্যভিচার, ভরনপোষন দেওয়ার অসমর্থ, ইত্যাদি। – ডিক্রি স্বামীকে নোটিশ না দিয়ে করা যাবে না, এই সময়ে নোটিশ জারি হবে। – ডিক্রি প্রদানের 6 মাস অতিক্রম না করলে কার্যকর হবে।

The Muslim Marriages and Divorces (Registration) Act, 1974

– বিবাহ বিচ্ছেদ এর এই আইনের ধারা ৬ এ বলা হয়েছে যে, বিবাহ বিচ্ছদ এর নিবন্ধন এর জন্য মৌখিকভাবে আবেদন করার পদ্ধতি |

বাংলাদেশে আপনার বিবাহ বিচ্ছেদ বা বিবাহের বিষয়ে সাহায্যের জন্য TRW এর আইনজীবী দের নিয়োগ করুন:

বাংলাদেশে তাহমিদুর রহমান রিমুরা ওয়াহিদ আইনী প্রতিষ্ঠান বিবাহ এবং বিবাহ বিচ্ছেদের বিষয়ে আইনি পরামর্শ প্রদান করে:

ঢাকা, বাংলাদেশের মহাখালী ডিওএইচএস-এ TRW-এর ব্যারিস্টার, অ্যাডভোকেট এবং আইনজীবীদের বিয়ে, বিবাহবিচ্ছেদ এবং ভরণপোষণের বিষয়ে ব্যাপক অভিজ্ঞতা রয়েছে। নিয়মিতভাবে গার্হস্থ্য ক্লায়েন্টদের মধ্যে বিবাহ এবং বিবাহবিচ্ছেদ সংক্রান্ত বিভিন্ন সমস্যাগুলি পরিচালনা করার পাশাপাশি, এটির অনেক আন্তর্জাতিক ক্লায়েন্টকে তাদের আইনি সমস্যায় পরম যত্ন এবং মনোযোগ দিয়ে পরামর্শ এবং সহায়তা করার অভিজ্ঞতা রয়েছে। আমাদের সাথে যোগাযোগ করুন:

ই-মেইল: info@tahmidur.com অথবা info@trfirm.com ফোন: +8801847220062 | +8801779127165

Unlocking Investment Potential in Bangladesh: Navigating IRR within Legal Frameworks of Bangladesh

In the realm of financial analysis and investment evaluation in Bangladesh, the Internal Rate of Return (IRR) stands as a fundamental metric that helps investors and businesses estimate the potential profitability of various investment opportunities.

The IRR is a critical tool in the toolkit of financial professionals, aiding in the assessment of projects, capital investments, and business ventures.

A compound interest rate calculated over the life of a private equity fund to reflect both the investment return and the rate at which the return is generated.

The IRR is calculated using an iterative mathematical formula that values the cash spent by the private equity provider (typically subscription monies for shares and loan stock in the new company) and cash returned (typically interest, dividends, share or loan stock redemptions, and share sale proceeds) at the date of exit.

The IRR is the discount factor that provides a net present value of zero when applied to these cash flows. It roughly corresponds to a notional rate of compound yearly interest earned on money invested.

What Is Internal Rate of Return (IRR)?

The Internal Rate of Return, commonly known as IRR, is a financial metric used to evaluate the potential returns of an investment. It is a discount rate that, when applied to the cash flows of an investment, makes the Net Present Value (NPV) equal to zero in a discounted cash flow analysis. In simpler terms, IRR is the annual rate of growth that an investment is expected to generate.

In Bangladesh, where the investment landscape is rapidly evolving, IRR serves as a crucial decision-making tool for both businesses and individuals. It allows investors to assess the attractiveness of various investment options, from real estate to business expansion, by providing a clear picture of the expected annual returns.

Formula and Calculation for IRR

The formula for IRR, though conceptually straightforward, often requires iterative calculations to determine the precise rate. In the context of Bangladesh, where investments vary widely in nature, understanding the IRR formula is essential.

The formula used to calculate IRR is as follows:

0 = Σ CFt ÷ (1 + IRR)^t

Where:

CFt = Net cash inflow during the period t

IRR = Internal Rate of Return

t = The number of time periods

In Bangladesh, this formula becomes particularly relevant when assessing investments that involve initial capital outlays, such as real estate development, infrastructure projects, or manufacturing ventures. The ability to determine the IRR helps investors gauge the profitability and feasibility of such endeavors.

Example of IRR Calculation in Bangladesh

Let’s consider a practical example of IRR analysis in Bangladesh using BDT as the currency. Imagine a company evaluating the profitability of a real estate project named Project X. Project X requires an initial investment of 2,500,000 BDT and is projected to generate annual after-tax cash flows as follows:

Year 1: 1,000,000 BDT

Year 2: 1,200,000 BDT

Year 3: 1,400,000 BDT

Year 4: 1,600,000 BDT

Year 5: 1,800,000 BDT

Using the IRR formula, one can calculate the IRR for Project X:

Solving this equation yields an IRR of approximately 12.29% for Project X. In the context of Bangladesh’s real estate sector, this IRR figure provides valuable insights into the project’s potential return on investment.

Unlocking Investment Potential in Bangladesh: Navigating IRR within Legal Frameworks

In the intricate tapestry of Bangladesh’s investment landscape, the Internal Rate of Return (IRR) emerges as a pivotal financial metric. However, as investors and businesses in Bangladesh engage in assessing potential projects and ventures, they must do so within the contours of the country’s legal and regulatory frameworks. In this exploration, we shall dissect the significance of IRR, its legal implications in Bangladesh, and how it interweaves with specific legal fields and terminology.

IRR: Legal Foundations and Application

The Internal Rate of Return (IRR) stands as a quintessential financial metric, both globally and in Bangladesh. It serves as a benchmark to evaluate the feasibility and profitability of investments, offering insights into the expected annual returns of a venture.

In Bangladesh, where investment opportunities span diverse sectors like real estate, infrastructure, and manufacturing, IRR plays a pivotal role in decision-making. It allows investors and businesses to gauge the financial viability of projects, taking into account various legal considerations.

Legal Fields and Considerations in IRR Analysis

Contract Law: One of the key legal fields that intertwine with IRR analysis is contract law. When assessing investment opportunities, contracts are integral, outlining the terms, obligations, and responsibilities of parties involved. Legal experts in Bangladesh play a crucial role in drafting and reviewing contracts, ensuring compliance with contractual obligations that impact cash flows and, subsequently, IRR.

Real Estate Law: The real estate sector in Bangladesh is burgeoning, attracting investors seeking to capitalize on the country’s growth. IRR calculations for real estate investments are inherently tied to land acquisition, property transactions, and land use regulations. Legal experts navigate the complexities of land ownership laws, ensuring that investments adhere to legal requirements, mitigating risks, and preserving IRR.

Taxation and Financial Law: In Bangladesh, tax implications significantly influence IRR. Income tax, capital gains tax, and value-added tax (VAT) obligations are paramount. Legal practitioners specializing in taxation ensure that IRR calculations incorporate accurate tax figures, optimizing returns and complying with the evolving tax regulations.

Foreign Investment Regulations: Bangladesh welcomes foreign investors, yet stringent regulations exist. Foreign investments often require approvals and compliance with regulatory bodies such as the Bangladesh Investment Development Authority (BIDA). Legal experts guide investors through the labyrinth of foreign investment laws, ensuring IRR calculations align with regulatory requirements.

Dispute Resolution: Bangladesh’s legal framework encompasses dispute resolution mechanisms. When investments face challenges or contractual disputes, legal experts in dispute resolution play a pivotal role in protecting investments and safeguarding IRR. Alternative dispute resolution methods are employed to minimize the impact on investment returns.

Legal Field

Role in IRR Analysis

Key Considerations

Contract Law

Drafting and reviewing contracts

Ensuring compliance with contractual obligations.

Real Estate Law

Land acquisition and property transactions

Verifying land titles, addressing disputes, and adhering to land ownership laws.

Taxation and Financial Law

Tax implications and financial compliance

Incorporating accurate tax figures and VAT obligations into IRR calculations.

Foreign Investment Regulations

Regulatory compliance for foreign investors

Guiding foreign investors through BIDA requirements and approvals.

Dispute Resolution

Managing investment disputes

Protecting investment returns through alternative dispute resolution methods.

Environmental Regulations

Environmental impact assessments (EIA)

Conducting thorough EIA studies and obtaining DoE approvals.

Political and Economic Stability

Risk assessment

Monitoring political and economic stability for informed investment decisions.

Infrastructure Development

Compliance with urban planning regulations

Aligning projects with zoning requirements and collaborating with local authorities.

Land Use Zoning and Planning

Land use regulations

Adhering to land use zoning laws and urban planning requirements.

Legal Documentation and Contracts

Contractual soundness

Ensuring contracts are legally sound and comprehensive.

Case Study: IRR in Bangladesh’s Real Estate Sector

Let’s delve into a real-world example to illustrate how IRR analysis intersects with these legal fields. Consider a foreign investor eyeing a real estate project in Bangladesh. The project involves acquiring land, constructing a commercial complex, and leasing space to local businesses. The investor conducts a comprehensive IRR analysis, factoring in legal considerations:

Land Acquisition: Legal experts verify land titles, conduct due diligence, and address any disputes or ambiguities. This diligence ensures that land acquisition aligns with land ownership laws and is a critical component of IRR calculations.

Contracts and Agreements: Lawyers draft contracts outlining the terms of land purchase, SPV contracts, SPA contracts, construction agreements, and lease agreements with tenants. Ensuring these contracts are legally sound and comprehensive is vital to safeguarding the IRR.

Taxation: Tax consultants assess the tax obligations tied to rental income, capital gains, and VAT. Accurate taxation figures are integrated into the IRR analysis, impacting the project’s financial viability.

Dispute Resolution: In the event of disputes with tenants, contractors, or regulatory bodies, dispute resolution mechanisms are activated. Legal professionals work diligently to protect the investment’s returns and minimize disruptions to the IRR.

In Bangladesh, the Internal Rate of Return (IRR) is not merely a financial metric; it is a compass guiding investors and businesses through a multifaceted legal landscape. The legal fields of contract law, real estate law, taxation, foreign investment regulations, and dispute resolution converge with IRR analysis, shaping investment decisions and outcomes.

As Bangladesh continues its journey of economic growth and development, the prudent application of IRR within the legal frameworks is paramount. Legal experts and financial analysts work hand in hand to optimize IRR, mitigate risks, and ensure investments align with regulatory requirements.

In essence, IRR in Bangladesh serves as a bridge between financial aspirations and legal realities, unlocking the nation’s investment potential while upholding the rule of law. In this dynamic and evolving investment environment, the harmonious synergy of finance and law paves the way for sustainable development and prosperity.

Using IRR in Bangladesh: Real-world Applications

In Bangladesh, where economic growth and infrastructure development are on the rise, the application of IRR is widespread and diverse:

Real Estate Investments: The booming real estate market in Bangladesh attracts investors seeking to maximize their returns. IRR analysis is employed to assess the profitability of real estate projects, whether they involve residential, commercial, or industrial properties. The higher the IRR, the more desirable the investment.

Infrastructure Projects: Bangladesh’s infrastructure development is a top priority, with projects ranging from road construction to power plants. IRR is instrumental in evaluating the financial viability of such endeavors, helping the government and private investors make informed decisions.

Business Expansion: Local businesses looking to expand or diversify their operations use IRR to compare different expansion opportunities. It assists in determining which project is likely to yield the highest returns.

Capital Budgeting: IRR is a vital tool for capital budgeting decisions. Companies can use it to compare the profitability of launching new operations versus expanding existing ones. For example, an energy company might utilize IRR to decide between opening a new power plant or renovating an existing one.

Stock Buyback Programs: Corporations often employ IRR to assess the attractiveness of stock buyback programs. It helps determine whether allocating funds to repurchase company shares generates a higher IRR than other uses of capital.

Challenges and Considerations

While IRR is a valuable tool in the financial arsenal, it is not without limitations. In Bangladesh, as in other countries, investors and businesses must be aware of these challenges:

Projections and Assumptions: IRR relies on estimates of future cash flows, making it sensitive to the accuracy of these projections. Investors should exercise caution and conduct thorough due diligence when making assumptions.

Multiple IRRs: In cases with unconventional cash flow patterns, IRR analysis may yield multiple IRRs, creating ambiguity. Careful interpretation and additional financial metrics may be necessary.

Comparison with WACC: IRR should be compared to the Weighted Average Cost of Capital (WACC). Projects with IRRs above the WACC are generally considered profitable. However, this comparison may not always be sufficient for longer-term projects with varying discount rates.

Scenario Analysis: To mitigate risks associated with IRR estimates, scenario analysis should be employed. Considering various scenarios helps assess the impact of changing assumptions on investment returns.

Hire the best Investment law firm for your upcoming project in Bangladesh:

On a global scale, the investment management business is currently undergoing tremendous regulatory upheaval. Tahmidur Rahman Remura Wahid TRW is well-positioned to address these issues for clients in investment management.

The business is made up of a broad group of players, ranging from corporations, financial institutions, and sovereign wealth funds to individuals, all of whom manage quite distinct and frequently disparate assets in accordance with very different strategies. A worldwide private equity firm’s needs, for example, are significantly different from those of a start-up hedge fund manager.

However, both confront the same investor expectations for improved performance. With the new world of heightened regulation and its extra-territorial application, as well as the increasing demands of investors for a more institutional approach, the job of an investment manager is more difficult than ever.

Our understanding of each component of the investment management industry, combined with our global network of expertise, enables us to tailor our advice to a client’s specific needs while also providing access to the most recent market thinking and advice from around the world, whether under Dodd-Frank or in relation to AIFMD or EMIR.

We provide advice on fund creation, licensing, taxation, transactional and M&A transactions, as well as contentious matters. We also provide advice on regulation affecting the investment management industry across financial markets, covering all current developments. With the help of expert lawyers from our global network, we can provide a global or local solution, including guidance on the impact of extra-territorial legislation in each jurisdiction.

We collaborate with our debt finance team to provide our clients with a complete capital financing platform. Our Fund financing practice advises lenders and borrowers on a wide range of fund-level financing solutions, as well as general partner facilities. Our experience includes capital call (subscription) bridge finance, leveraged NAV facilities, and hybrid financing, which may include preference interests, securitisation treatment, or other specialized solutions.

Our clientele include some of the world’s most prestigious asset management firms, alternative investment funds, private equity funds, insurance organizations, and private banking firms. They range in size from multinational corporations with a five-continent presence to start-up or spin-off funds.

GLOBAL OFFICES: DHAKA: House 410, ROAD 29, Mohakhali DOHS DUBAI: Rolex Building, L-12 Sheikh Zayed Road LONDON: 1156, St Giles Avenue, 330 High Holborn, London, WC1V 7QH