Land ownership and property rights hold immense significance in any society, providing stability and security to individuals and communities.

In Bangladesh, where land is a precious resource and a crucial element of livelihoods, the accuracy of land records is of paramount importance. A Khatian, a document that records land ownership details, serves as the cornerstone for property transactions and legal disputes.

However, discrepancies or errors in Khatians can lead to confusion, disputes, and injustices. To address these issues, the legal system in Bangladesh provides the avenue of a Khatian correction suit. In this article, we delve into the intricacies of Khatian correction suits, highlighting their significance, procedures, and challenges.

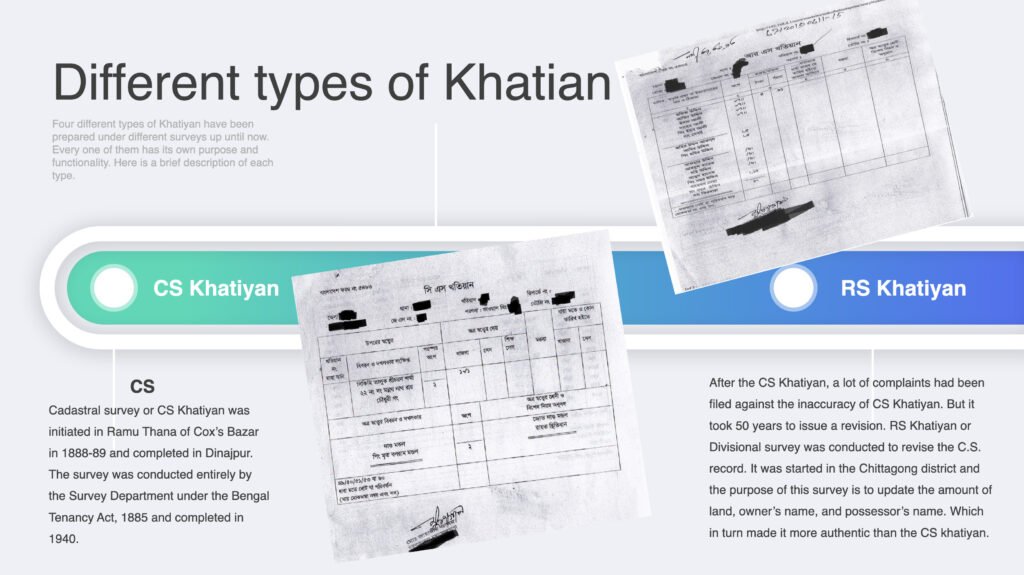

Understanding Khatian and Its Importance

In the context of land ownership, a Khatian is a vital document that establishes the legal identity of land parcels, their boundaries, and the respective owners. It serves as a comprehensive record of rights, tenures, and liabilities associated with land.

Accurate Khatians are essential for various purposes, including property transactions, inheritance, dispute resolution, and land development. When Khatians contain errors or inaccuracies, it can lead to misunderstandings, legal battles, and hinder socio-economic progress.

CONTENTS OF KHATIAN

Khatiyan determines a lot of critical factors. It does not determine the right to possession of the land, but it serves as supporting evidence for the Title Deed (another vital document for validating ownership). A Khatiyan, or Record of Rights, comprises the following information to that end:

Khatian number;

Mouza,Upazilla, District and J.L.No;

Name, father’s name and address of the owner or owners;

Plot (dhag) number;

Portion of the owner or owners;

Class and nature of the land;

Amount of land development tax payable;

Total amount of land (dhag wise) etc.

The Need for Khatian Correction Suits

Errors in Khatians can occur due to a variety of reasons, including typographical mistakes, inaccurate surveys, boundary disputes, and illegal land encroachments. These errors can result in wrongful dispossession of land, disputes among co-owners, and difficulties in obtaining loans or grants.

To address such issues and ensure equitable land ownership, the legal system in Bangladesh provides the option of filing a Khatian correction suit.

Initiating a Khatian Correction Suit

A Khatian correction suit is a legal remedy available to individuals or parties seeking to rectify errors or inaccuracies in land records. The process involves several stages:

Gathering Evidence: The plaintiff (the party initiating the suit) needs to collect substantial evidence that demonstrates the errors in the Khatian. This may involve land survey reports, affidavits from witnesses, historical documents, and any other relevant records.

Filing the Suit: The plaintiff files a suit in the appropriate court, usually the relevant Subordinate Judge Court or Assistant Judge Court, within the jurisdiction where the land is located. The suit should include details of the errors, the proposed corrections, and the grounds for correction.

Summons and Notice: Once the suit is filed, the court issues summons to the defendant(s), notifying them about the lawsuit and its nature. The defendants are given the opportunity to respond and present their side of the case.

Evidence and Arguments: Both parties present their evidence and arguments before the court. The plaintiff must establish the existence of errors in the Khatian, while the defendant may counter with evidence supporting the accuracy of the document.

Court’s Decision: After evaluating the evidence and hearing the arguments, the court decides whether the corrections requested by the plaintiff are justified. If the court deems the corrections necessary, it will issue an order directing the relevant authorities to make the necessary amendments to the Khatian.

Challenges and Considerations

Navigating a Khatian correction suit can be a complex and time-consuming process, involving legal intricacies and potential challenges:

Evidence Collection: Gathering compelling evidence to substantiate errors in the Khatian is essential. This often requires thorough research, land surveys, and witness testimonies, which can be resource-intensive.

Legal Expertise: Engaging legal counsel with expertise in property law is advisable to navigate the legal complexities and procedural requirements of the correction suit.

Delays and Backlogs: The judicial system in Bangladesh, like many other countries, may experience delays and backlogs. This can prolong the duration of the suit, causing frustration and additional costs.

Cooperation of Authorities: The cooperation of relevant land authorities and government agencies is crucial for implementing the corrections ordered by the court. Delays or reluctance on their part can hinder the effectiveness of the correction process.

Boundary Disputes: If the errors in the Khatian are related to boundary disputes, resolving these disputes may require negotiations and consensus-building among the parties involved.

Khatian correction suits play a vital role in ensuring accurate land records, equitable land ownership, and the prevention of unjust dispossession. In a country like Bangladesh, where land-related conflicts can have far-reaching socio-economic implications, a robust and effective mechanism for correcting Khatian errors is essential. By understanding the process, challenges, and potential benefits of filing a Khatian correction suit, individuals and communities can take steps towards securing their land rights, resolving disputes, and contributing to a more just and prosperous society.

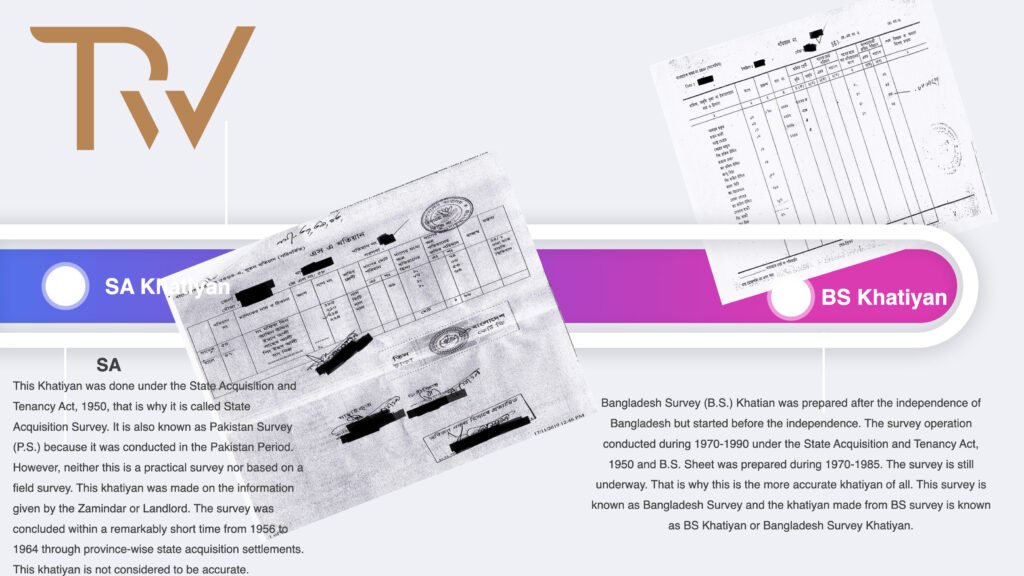

State Acquisition and Tenancy Act – SAT ACT

State Acquisition and Tenancy Act; which is specially created for resolving disputes originating from the final publication of the last revised record-of-rights prepared pursuant to Section 144 of the SAT Act.

On the basis of this research and a certain amount of experience with it, we have determined that a large number of cases have been lodged before it without the Tribunal’s knowledge.

The provisions of I 45A(1) make it plain that the Land Survey Tribunal is to be established to correct only the most recently revised record of rights, i.e. only the BS, BRS, or RS record. Therefore, such Tribunals will only have the authority to rectify the final BRS record; they will not be able to view information beyond the final record.

In this regard, Section 145A(4) of the SAT Act may be quoted: “The Land Survey Tribunal shall have no jurisdiction over any action other than those arising from the final publication of the last revised record of rights prepared pursuant to Section 144.”

This subsection (4) of section 145A states that the Tribunal shall only have jurisdiction over cases arising from the final publication of the “last revised record of rights,” i.e. the BS/ BRS/RS Khatian. Therefore, in the Land Survey Tribunal, only the most recent record-of-rights can be the subject of a lawsuit.

Entering in the recent record-of-rights:

Additionally, we are aware that the last (BRS) record cannot be rectified unless the SA record in the plaintiff’s or his predecessors’ names is corrected. Referencing “Without correcting the SA Khatian and RS Khatian as prepared for the case lands in accordance with law previously, the petitioner cannot get its name entered in the recent record-of-rights prepared during the Mohanagar Survey allegedly solely on the basis of CS Khatian” is permissible in this regard.

The petitioner had no standing to dispute the draft Mohanagar Survey Khatian prepared in the names of the respective writ petitioners, at least after the publication of the gazette notifications dated 24 March 1952 and 29 February 1956″, 15 BLC (AD) 115.

Reading this section 145A from this perspective, it is also presumed that the Land Survey Tribunal lacks the authority to correct the SA record; in other words, if a dispute in a lawsuit involves the incorrectness of the former SA record, the Land Survey Tribunal shall have jurisdiction to hear the lawsuit under section 110.

The term ‘arising out of’ as used in this subsection (4) does not include any action in which the plaint alleges that the last BS record was incorrectly published, thereby casting a cloud over the plaintiff’s title.

These terms should only refer to those that the Tribunal may grant pursuant to subsection (8) of section 145A of the SAT Act, i.e. only the correction of the record of rights.

Consequently, suits which, in their petition, seek a declaration that the most recent BS record is incorrect and also seek correction of the said BS record in a specified manner shall be deemed to arise from the most recent record of rights.

Though a suit in the Land Survey Tribunal is not a writ petition, as we have already observed, this is clearly a summary proceeding.

Land Survey Tribunal and summary proceedings

As a result, we presume that the above-mentioned writ principle that “when a dispute involves a complicated question of title and possession between the parties, then this dispute cannot be determined in Land Survey Tribunal in a summary proceeding; rather, the matter should be determined by a civil court in a properly formed suit for establishment of title of the parties” will provide support for our position.

We find support for the following viewpoint: – A right of easement to be confirmed in a proceeding under section 143A is completely outside the scope of investigation under this section, 31 DLR 421. The Court below should exercise caution in encouraging adjudication of disputed title and possession under the auspices of a procedure under Section 143A. A fully effective adjudication of title and possession must be left open for a properly organized suit, 31 DLR 42 J.

In this connection, Section 54 of the SAT Act makes it explicit that where the parties disagree over title to and possession of the suit lands, the Land Survey Tribunals have no authority to settle the disagreement. Only the Civil Court has the authority to proclaim title to and possession of the suit lands.

This point of view is supported by decisions published in 10 DLR 527, 53 DLN 506, and BSCD Vol. Vp. 269. The suit contemplated in Section 30 of the SAT Act is not a suit for the determination of a question of title and possession.

The bar of jurisdiction created by Section 30(2) of the SAT Act is unrelated to the question of title and possession to any land, which is expressly dealt for in Section 54 of the Act, 10 DLR 527.

FAQs about Khatian Correction Suits in Bangladesh

What is a Khatian?

A Khatian is a document that records land ownership details, boundaries, and related information. It serves as a vital record for property transactions and legal purposes in Bangladesh.

Why might I need to file a Khatian correction suit?

You might need to file a Khatian correction suit if there are errors, inaccuracies, or disputes related to land ownership or boundaries in the Khatian document.

Where do I file a Khatian correction suit?

Khatian correction suits are usually filed in the relevant Subordinate Judge Court or Assistant Judge Court within the jurisdiction where the land is located.

What evidence do I need to gather for the suit?

You need to gather evidence that substantiates the errors or inaccuracies in the Khatian. This may include land survey reports, affidavits, historical documents, and other relevant records.

Do I need a lawyer to file a Khatian correction suit?

While not mandatory, it’s advisable to engage a lawyer with expertise in property law to navigate the legal complexities and ensure a strong case presentation.

What is the process of filing a Khatian correction suit?

The process involves filing the suit, serving summons and notice to the defendant(s), presenting evidence and arguments, and awaiting the court’s decision on the corrections requested.

What if the defendants dispute the corrections?

If the defendants dispute the corrections, they can present their evidence and arguments in court. The court will evaluate both sides before making a decision.

How long does the process typically take?

The duration of a Khatian correction suit can vary. Delays in the judicial system, evidence collection, and other factors may impact the timeline.

What happens if the court approves the corrections?

If the court approves the corrections, it will issue an order directing the relevant authorities to make the necessary amendments to the Khatian document.

Can a Khatian correction suit resolve boundary disputes?

Yes, a Khatian correction suit can be used to address boundary disputes by presenting evidence and seeking a court-mandated resolution.

What challenges might I face during the process?

Challenges include evidence collection, potential delays in the legal system, cooperation from authorities, and negotiating with other parties involved.

Can I appeal the court’s decision if I’m dissatisfied?

Yes, you have the right to appeal a court decision if you are dissatisfied with the outcome of the Khatian correction suit.

How can I ensure accurate land records in the future?

Regularly monitoring and verifying your Khatian, updating information as needed, and maintaining accurate land records can help prevent future disputes.

Contact the best land lawyers and property law firm in Bangladesh:

GLOBAL OFFICES: DHAKA: House 410, ROAD 29, Mohakhali DOHS DUBAI: Rolex Building, L-12 Sheikh Zayed Road LONDON: 1156, St Giles Avenue, 330 High Holborn, London, WC1V 7QH

Company Registration in Bangladesh: A Comprehensive Guide

Registering a company in Bangladesh is a crucial step for investors looking to start a business or expand their operations in the country. Bangladesh offers a favorable environment for company registration procedure in bangladesh, and most businesses prefer to be registered as private limited liability companies due to the legal protection and limited liability they offer.

In Bangladesh you can do proprietorship company registration in bangladesh, private limited company or if you are a foreign entity then you can incorporate your fully owned subsidiary, branch or liaison office in Bangladesh by hiring suitable company registration consultants in bangladesh.

This article from our esteem partners aims to provide a detailed overview of the company registration process in Bangladesh, requirements, and post-registration formalities in Bangladesh for private limited company incorporation in Bangladesh.

Pre-Registration – What You Need to Know

Before diving into the company registration process, it’s essential to understand key facts about company formation in Bangladesh:

Company Name Clearance: The proposed company name must be approved (cleared) before incorporation.

Directors: A minimum of two directors are mandatory, who can be either local or foreign. Directors must be at least 18 years old, not bankrupt, and not convicted of malpractice in the past. They must own qualification shares as stated in the Articles of Association.

Shareholders: A private limited company can have a minimum of 2 and a maximum of 50 shareholders. Shareholders can be individuals or legal entities.

Authorized Capital: The maximum share capital the company is authorized to issue must be stated in the Memorandum of Association and Articles of Association.

Paid-up Capital: The minimum paid-up capital for registration is Taka 1, but it can be increased after incorporation.

Registered Address: A local address must be provided as the registered address, which must be a physical address and not a P.O. Box.

Memorandum and Articles of Association: The company must prepare these two documents detailing the business objectives, shareholder information, and company regulations.

Considerations for Foreigners

Foreign investors planning to register a company in Bangladesh i.e a foreign company registration in bangladesh, should take note of the following points:

Bank Account Opening: A bank account must be opened in the name of the proposed company with the name clearance obtained from the Registrar of Joint Stock Companies and Firms (RJSC).

Remote Incorporation: All incorporation formalities can be handled remotely through authorized lawyers/agents in Bangladesh.

Foreign Directors and Shareholders: All directors and shareholders can be foreigners, and there is no requirement for any special visa if they do not plan to relocate to Bangladesh.

Work Permit: If foreign investors plan to operate the company from Bangladesh, they must obtain a work permit.

Required Documents

At first, before we get into the process of company registration in bangladesh, for company incorporation in Bangladesh, the following documents are required by the company registrar:

Company Name Clearance Certificate

Memorandum of Association and Articles of Association

Shareholders’ particulars (National ID for Bangladeshi shareholders)

For foreigners: Copy of passport of shareholders and directors.

Procedure for Company Registration in Bangladesh

The company registration process in Bangladesh involves the following steps:

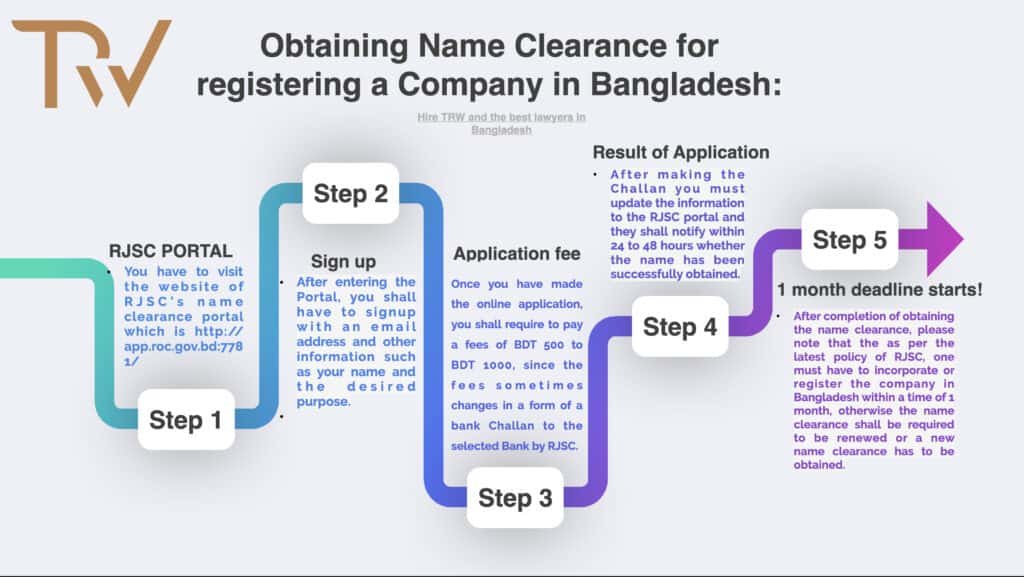

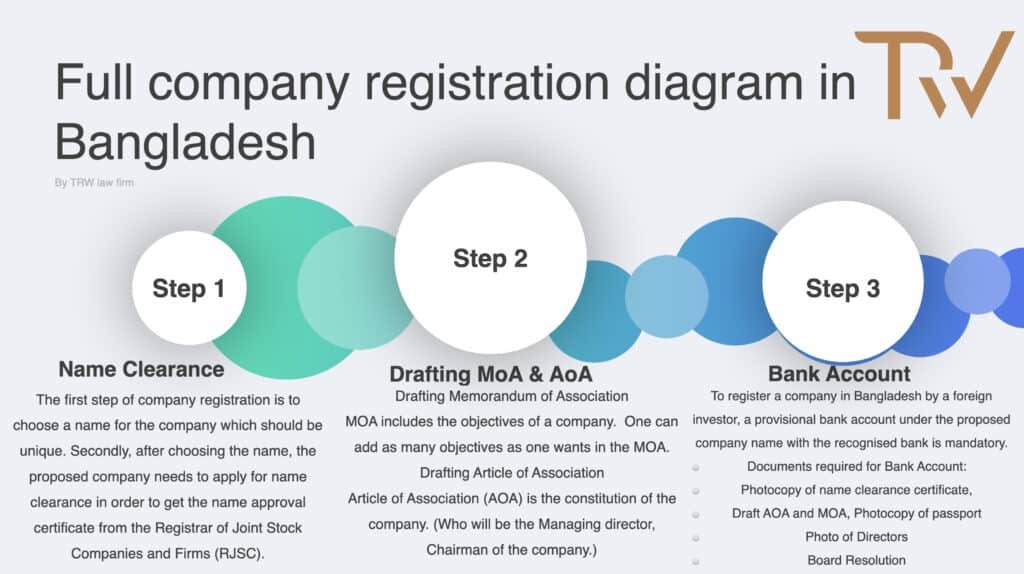

Step 1: Name Clearance

Select a desired company name and apply for name clearance on the Registrar of Joint Stock Companies and Firms (RJSC) website.

Pay the prescribed fee for name clearance.

After verification, RJSC will issue a name clearance certificate, which is valid for six months and can be extended if necessary.

Step 2: Drafting AoA & MoA for company registration in bangladesh

Drafting Memorandum of Association:

A limited company’s Memorandum of Association (MOA) is an essential aspect of the company registration process. A company’s objectives are included in a MOA. In the MOA, you can include as many objectives as you wish.

Drafting Article of Association:

The company’s constitution is its Articles of Association (AOA). As a result, the AOA contains all of the regulations governing how a limited company will operate, as well as who will serve as the firm’s Managing Director, Chairman, and Directors.

Step 3: Bank Account Opening and Paid-up Capital

Open a temporary bank account in the company’s name with a scheduled bank in Bangladesh.

Remit the paid-up capital (if foreign shareholding) to the bank account, and obtain an Encashment Certificate from the bank.

Deposit of share capital:

Following the opening of the provisional bank account, for completing company registration in bangladesh, a share money deposit will be paid from the foreign shareholder’s nation to the provisional account. As a result, the funds must be transferred from the shareholder’s person or entity account. After receiving payment, the Bangladeshi bank will provide an encashment certificate.

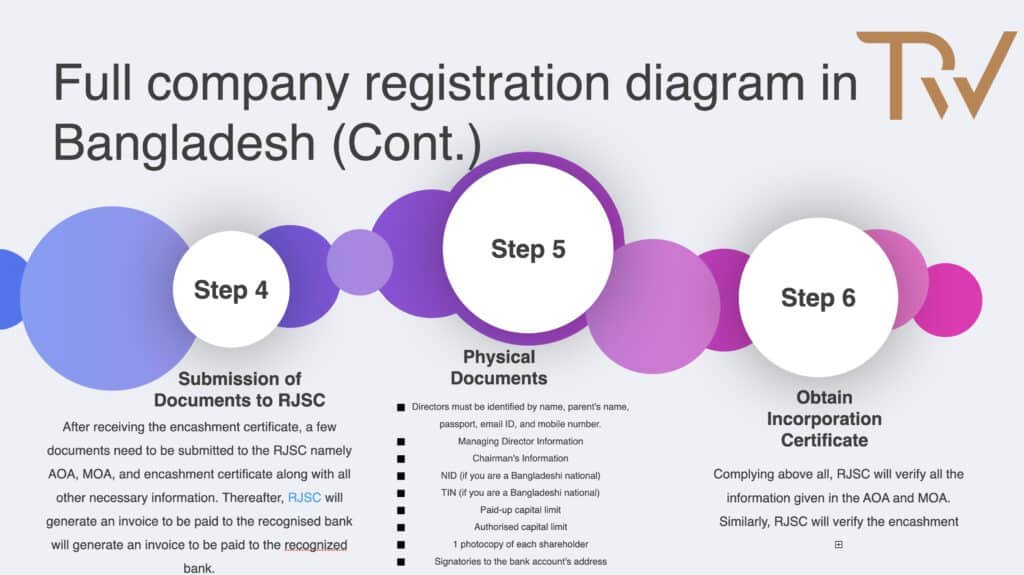

Step 4: Submit Company Information to RJSC

Upload digital copies of the MoA, AoA, and other required documents on the RJSC website.

Step 5: Submission of Physical Documents and required fee

Affix non-judicial stamps on the MoA and AoA.

Submit physical copies of the MoA, AoA, and other documents, along with the Encashment Certificate, to RJSC.

The government registration fee is determined by the company’s authorized capital. For example, if the allowed capital is 50 lakh, the government charge will be BDT 13570 (USD 160) plus 15% VAT. The government fee for company registration in Bangladesh can be found here.

Step 6: Obtain Incorporation Certificate

RJSC officials will review the submitted documents.

If satisfied, RJSC will issue the Certificate of Incorporation, Digital Certified Copy of MoA and AoA, and List of Directors (Form XII).

Present the Incorporation Certificate to the bank to convert the temporary account to a regular account.

Post-Registration Formalities

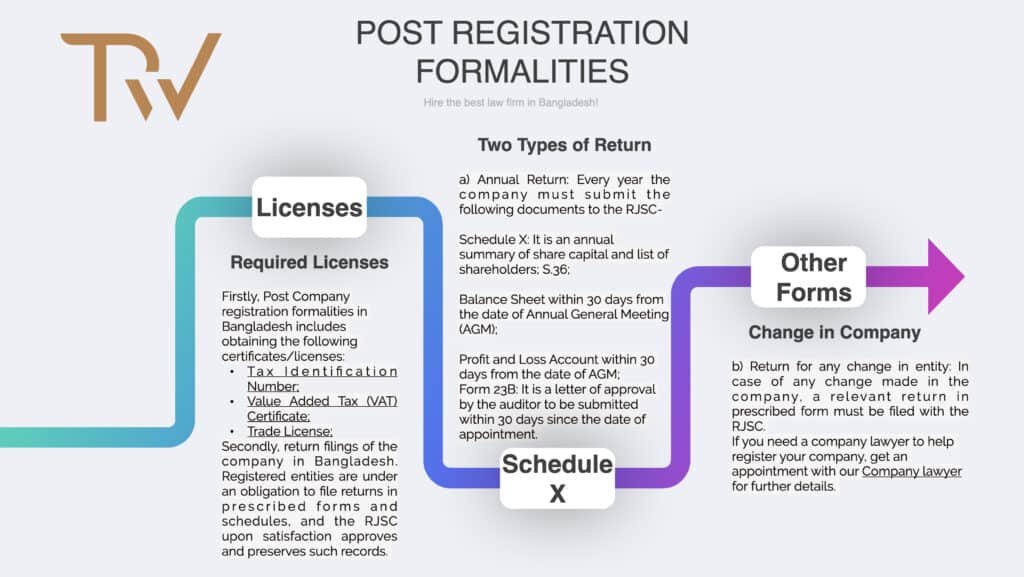

After company registration, the following post-registration formalities need to be completed:

Obtain Trade License, Tax Identification Number, and Other Licenses: Apply for a trade license and obtain a Tax Identification Number (TIN). Depending on the business activities, additional licenses may be required.

Return Filing Requirements:

Annual Return:

Hold an Annual General Meeting (AGM) within 18 months of incorporation, and no more than 15 months between subsequent AGMs.

Regular Return:

File relevant returns for any changes in the board of directors, shareholding structure, or other significant changes.

Taxation and Company Registration in Bangladesh:

Corporate Tax Rate

Applicable Companies

25%

Publicly traded companies (listed companies on the stock market)

30%

Non-publicly traded companies (private companies limited by shares)

37.5%

Publicly traded banks, insurance, and financial institutions other than merchant banks

40%

Non-publicly traded banks, insurance, and financial institutions

40%

Publicly traded mobile network operators

45%

Non-publicly traded mobile network operators

45%

Publicly traded cigarette manufacturers

45%

Non-publicly traded cigarette manufacturers

25%

One Person Company (OPC)

Taxation Process

Annual Income Tax Return Deadline

File income tax return annually

Usually on 15th January of the next year following financial closing (usually July-June).

Additional Tax Information

What is the Corporate Tax on profit?

Corporate tax on its profit Minimum tax usually @ 0.06% of gross revenue to be paid

How to Inject paid-up capital to the company’s bank account?

By cheques or any other instrument

Are there any transparency requirement?

The company should adequately explain debit-credit in the bank statements

Please note that besides the corporate tax rates mentioned above, there are several tax exemption facilities available for companies based on the nature of their business and location. Additionally, one-person company registration in Bangladesh has been officially launched, allowing individuals to incorporate a company on their own.

FAQ about Company Registration in Bangladesh:

FAQ

Answer

What is a Private Limited Company?

A Private Limited Company is a type of company that restricts the right of share transfer, limits the number of members to fifty, and prohibits public invitation to subscribe to shares or debentures.

How to incorporate a private limited company?

The process of company registration in bangladesh involves obtaining name clearance, drafting required documents, opening a temporary bank account, submitting documents to RJSC, and obtaining the incorporation certificate.

Are there any minimum shareholders required to form a company?

Yes, a minimum of two shareholders is required to form a private limited company.

Are there any minimum directors required to form a company?

Yes, a minimum of two directors is required to form a private limited company.

Is there any requirement of a resident/local director to operate a foreign company in Bangladesh?

Generally, there is no requirement for a resident/local director, but one director must be physically present to open a bank account.

Is there any minimum amount for the authorized and paid-up capital to be prescribed?

There is no specific limit on authorized or paid-up capital, but it is suggested to have a minimum authorized capital equivalent to USD 50,000 for legal purposes and adequate paid-up capital for business operation.

Are there any guidelines on reflecting company activities in the name?

There are no strict guidelines, but it is suggested to reflect the company’s activities in the name.

Is it mandatory to have a registered local address for the company?

Yes, a registered local address is mandatory for the company.

Do you provide office address?

Yes, office address services are available for company registration.

What documents are required for company formation?

Required documents include Memorandum of Articles and Articles of Association, directors’ resolution, consent forms, and various registration forms.

Whether prior permission of regulatory authority is needed for making investment?

For investment in kind, the concerned company needs to be registered with RJSC, and relevant forms and agreements must be filed with RJSC for record-keeping.

What is the difference between authorized capital & paid-up capital?

Authorized capital is the maximum share capital the company can issue, while paid-up capital is the amount actually paid by shareholders.

Whether directors need to obtain any registration before becoming directors of the company?

Directors do not need any specific registration before becoming directors.

Is it mandatory to appoint a company secretary?

There is no mandatory requirement for a company secretary in private limited companies.

What is the timeline for company formation?

The timeline for company formation may vary, but it usually takes a few weeks to complete the entire process.

What are the post-company formation required licenses and approvals?

Post-formation, licenses such as Tax Identification Number (TIN), Trade License, and VAT Registration Certificate need to be obtained.

When will a company be fully ready to operate legally in Bangladesh?

A company can start operating legally in Bangladesh after completing the registration process and obtaining necessary licenses and approvals.

Are there any restrictions/guidelines for altering company operation & management in the future?

Yes, any changes in company operation or management must be reported to the Company House.

What documents are required for bank account opening?

Documents such as the Certificate of Incorporation, Memorandum and Articles of Association, and identification documents are required for bank account opening.

Can a company own several businesses under different names?

Yes, a company can own multiple businesses under different names, as long as it complies with its Memorandum of Association and obtains necessary permissions if required.

Can a company change its business category not mentioned in its memorandum?

To carry out a different business not mentioned in the memorandum, the company needs to apply to the High Court to add that category.

Registering a company in Bangladesh is a streamlined process that can be handled remotely through authorized agents. Foreign investors have the flexibility to operate their businesses from overseas or relocate to Bangladesh with appropriate work permits. With its investor-friendly policies and favorable business environment, Bangladesh presents attractive opportunities for both local and foreign entrepreneurs.

If you are considering company registration in Bangladesh, it is advisable to seek professional legal assistance to navigate the registration process efficiently and ensure compliance with all regulatory requirements.

Time Requirement For A Company Formation

We want to finish the registration procedure as soon as possible. Preparing papers, RJSC online filing, payment, and a physical encounter with RJSC might also affect the timeline.

The fees and costs of company registration in Bangladesh will be determined by the nature of your firm. The following table shows the projected cost of forming a company:

Category

Nature of Business

Expected Cost (Taka)

A

Service and General Trading Company

Less than 60000

B

Relating to Export and Import Company

Less than 120000

C

Relating to Export, import and Manufacture

Less than 400000

D

Branch and Representative Office

Less than 60000

E

Employment and Investor Visa

Less than 50000

Summary for Company Registration in Bangladesh and FAQ:

Are you planning to do your company registration in Bangladesh?

Company formation and registration at Tahmidur Rahman Remura Wahid: The Law Firm in Bangladesh:

The legal team of Tahmidur Rahman Remura Wahid Law Firm in Bangladesh are highly experienced in providing all kinds of services related to forming and registering all sorts of companies in Bangladesh . For queries or legal assistance, please reach us at:

E-mail: info@trfirm.com Phone: +8801847220062 or +8801779127165

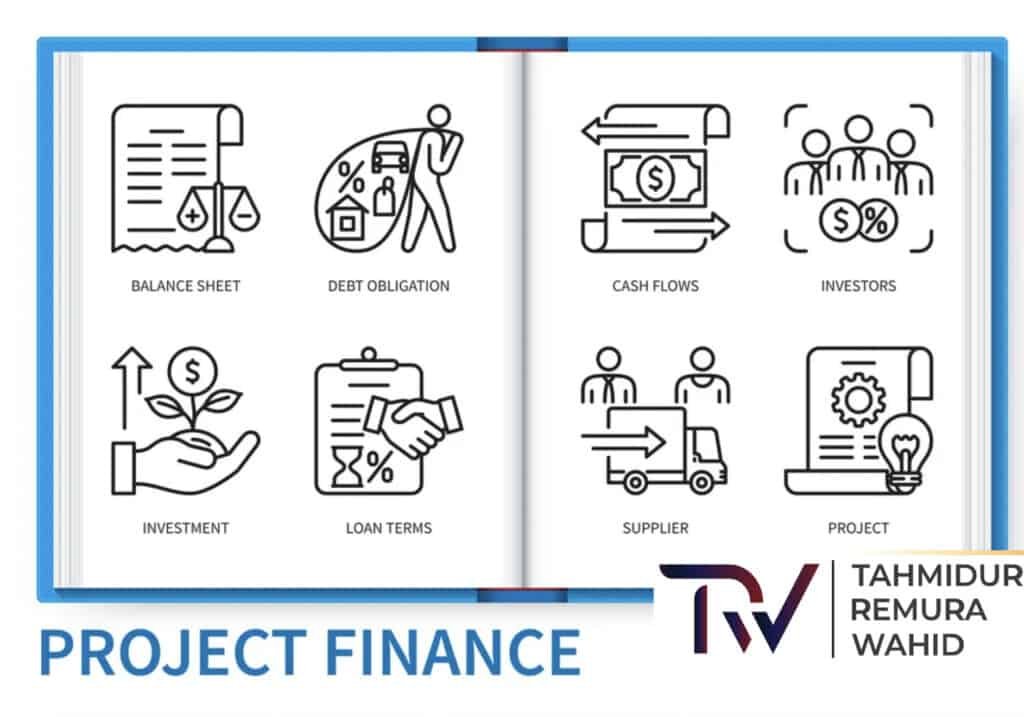

Industrial Project Finance in Bangladesh: A Comprehensive Guide

Industrial project finance is a vital component driving economic development and infrastructure growth in Bangladesh.

This financing mechanism plays a crucial role in funding industrial and infrastructure projects, fostering economic growth, and enhancing the country’s competitiveness.

In this comprehensive guide presented on behalf of the Tahmidur Rahman Remura law firm, we will delve deeper into the intricacies of industrial project finance in Bangladesh, including the types of projects financed, regulatory framework, approval requirements, material laws, international treaties, and structuring the financing.

Types of Projects Finance in Bangladesh:

Industrial and infrastructure projects are the primary beneficiaries of project finance in Bangladesh. Industrial projects, predominantly concentrated in the private sector, encompass diverse sectors such as manufacturing, textiles, garments, pharmaceuticals, and more.

These projects fuel the industrial growth of the nation, creating job opportunities and contributing to the overall economic landscape.

On the other hand, infrastructure projects are often undertaken either by the government of Bangladesh itself or through public-private partnership (PPP) models.

These essential projects include toll roads, ports, metro rail systems, liquified natural gas (LNG) terminals, power generation facilities, and energy initiatives.

They address critical infrastructure needs, facilitating efficient transportation, energy distribution, and enhancing the overall quality of life for citizens.

Additionally, project finance is extended to service sectors, such as education, healthcare, telecommunications, and other emerging industries that contribute significantly to the country’s progress.

Regulatory Framework for Project Finance in Bangladesh:

The regulatory framework for industrial project finance in Bangladesh is a crucial aspect that ensures transparency, compliance, and accountability throughout the financing process. Key regulatory authorities involved in project finance approvals include:

Bangladesh Bank:

As the central bank and the supreme regulatory authority for financial matters, Bangladesh Bank plays a pivotal role in approving project finance applications. It sets guidelines and regulations for both local and foreign currency borrowing and oversees the smooth functioning of the financial sector.

Bangladesh Investment Development Authority (BIDA):

BIDA is the government authority responsible for processing loan applications authorized by Bangladesh Bank. It evaluates and approves project proposals based on their economic viability, financial feasibility, and adherence to regulatory guidelines.

Executive Committee of the National Economic Council (ECNEC):

ECNEC, comprising all members of the Cabinet, approves major development projects, including infrastructure initiatives. It plays a critical role in shaping the nation’s long-term economic development policies and priorities.

Economic Relations Division (ERD):

ERD, under the Ministry of Finance, mobilizes external resources for socio-economic development. It approves sovereign guarantees or framework agreements with foreign lenders or governments, ensuring adherence to international norms and regulations.

Bangladesh Securities and Exchange Commission (BSEC):

BSEC is responsible for approving issues of bonds by private entities and overseeing large-scale share offerings. It ensures compliance with securities laws and regulations, safeguarding the interests of investors and stakeholders.

Regulatory Considerations and Approval Requirements

To facilitate industrial project finance, Bangladesh has established specific regulatory considerations and approval requirements for both local and foreign currency borrowing.

Local Currency Borrowing:

Local banks and financial institutions can extend loans to local companies in Bangladeshi Taka (BDT). Approved forms of local currency lending include continuous loans (cash credit, overdrafts, etc.), demand loans (e.g., loans against imported merchandise), and fixed-term loans.

The Bangladesh Bank sets a limit on the interest rate spread between deposits and lending (currently around 9%). Lenders must maintain risk-based capital adequacy and adhere to single borrower exposure limits to mitigate risks.

Additionally, lenders must verify borrowers’ credit information from the Credit Information Bureau before authorizing, renewing, or rescheduling loans, ensuring that credit facilities are not provided to defaulters. Credit risk grading is adopted for large loans to assess credit risk effectively.

Foreign Currency Borrowing:

Public sector companies must obtain authorization from ECNEC and approval from ERD for foreign loans.

Any sovereign guarantee or framework agreement with foreign lenders or governments must also be approved by ERD. Under local foreign exchange regulations, public sector companies require permission from the Hard Term Loan Sanction Department of Bangladesh Bank to receive hard term offshore loans. Generally, any interest rate of 4% or more is considered a hard term loan.

For private sector companies, the Bangladesh Bank requires borrowers to obtain permission from BIDA for foreign borrowing. Foreign loans can be raised from internationally recognized sources such as international banks, international capital markets, multilateral financial institutions, export credit agencies, and suppliers of equipment.

However, foreign borrowing is allowed for project financing purposes only and cannot be utilized as working capital. During the approval process, BIDA considers the borrower’s past conduct and the financial viability and profitability of the project.

Specific conditions applicable to foreign borrowing include a maximum 70:30 debt-to-equity ratio, with some sectors like power having an allowance of up to 80:20. The standard interest ratio is up to LIBOR +4%, with an all-in cost ceiling that considers interest and other annualized fees and expenses.

Shareholder Loans and Bonds:

Generally, shareholder loans for project financing are not allowed, except for short-term bridging purposes. Private sector entities can raise funds through bonds with the prospectus approved by BSEC and underwritten by a merchant bank.

Filing and Registration:

Local borrowing does not require registration. However, for foreign borrowing, the industrial or infrastructure project must be registered with BIDA before submitting the foreign borrowing application. All securities over immovable properties require registration with the office of the sub-registrar in the relevant geographic area.

In addition, securities over any asset of a company must be perfected with the Registrar of Joint Stock Companies (RJSC) within 21 days of the date of creation of the security. Certain conditions may also be imposed under concession agreements.

Material Laws and International Treaties

The legal landscape surrounding industrial project finance in Bangladesh is governed by various material laws and international treaties. Key material laws include:

This Act regulates foreign exchange transactions, including foreign borrowing, and sets guidelines for conducting such transactions in compliance with international norms.

These are rules formulated by the Bangladesh Bank, outlining the guidelines for foreign exchange transactions and ensuring proper adherence to regulations.

The Companies Act governs several aspects relevant to project finance, including the perfection of charges on a company’s assets, debt and equity conversions, and procedural compliances related to borrowing and security interest creation.

This Act provides summary procedures to enforce securities and loan agreements by local financial institutions and some foreign creditors such as the International Finance Corporation, Islamic Development Bank, World Bank, etc.

The CPC governs the procedure for civil court proceedings and is used by creditors for recovery proceedings and enforcement of security.

In addition to material laws, several international treaties to which Bangladesh is a party can affect cross-border transactions, including investment-related disputes, recognition, and enforcement of foreign arbitral awards, free trade agreements, comprehensive economic partnership agreements, and preferential trade agreements.

Structuring the Financing in Bangladesh

The successful structuring of industrial project finance in Bangladesh requires careful consideration and coordination among various parties involved in the transaction. Each party plays a distinct role in ensuring the smooth execution of the project and mitigating risks. Below are the main parties involved in an industrial project finance transaction:

Sponsors:

The sponsors are the owners or ultimate beneficiaries of the project. They initiate the project, bear the initial costs, and assume the risks associated with the venture. Sponsors are often responsible for bringing together the various stakeholders and securing financing for the project.

Project Company/Borrower:

The project company, also known as the borrower, is the entity responsible for implementing the project. It is typically a special-purpose vehicle (SPV) incorporated by the sponsors solely for the purpose of undertaking the project. The SPV isolates the project’s assets and liabilities from the sponsors’ other business activities, minimizing their exposure to potential risks.

Lender:

The lender, often a financial institution or consortium of lenders, provides the funds necessary for financing the project. Lenders assess the project’s feasibility, creditworthiness of the sponsors, and the anticipated cash flow from the project to ensure the repayment of the loan.

Off-taker:

The off-taker is the party, usually a government authority or state-owned enterprise, that enters into a long-term agreement with the project company to purchase the output or services generated by the project. For infrastructure projects, the off-taker is often the government agency responsible for that particular sector, such as the Bangladesh Power Development Board for power generation projects.

Third-Party Guarantors:

Third-party guarantors are entities other than the sponsors who provide guarantees to lenders for the repayment of the loan or fulfillment of the project’s obligations. These guarantees enhance the project’s creditworthiness and reduce the lender’s risk exposure.

Bank Guarantors:

Bank guarantors are financial institutions that issue performance or payment guarantees on behalf of the project company to support the project’s contractual obligations and mitigate potential risks.

Export Credit Agencies:

For projects involving the import of equipment and technology, export credit agencies (ECAs) can provide financing or insurance to exporters and lenders to facilitate cross-border transactions and mitigate commercial and political risks.

Security Trustee:

The security trustee is a resident entity appointed by the lenders to hold the project’s security interests on their behalf. The security trustee ensures that the lenders’ rights and interests are adequately protected and enforced in case of default.

Account Bank:

The account bank is the financial institution where the project company maintains an account to receive loan proceeds and accumulate funds for debt servicing and other project-related expenses.

Inter-Creditor Agent:

In syndicated financing, where multiple lenders are involved, an inter-creditor agent represents the lenders’ interests and facilitates coordination among them. The agent ensures that all lenders are treated fairly and that the syndication process runs smoothly.

Industrial project finance is a crucial driver of economic development and infrastructure growth in Bangladesh. The regulatory framework, supported by various authorities, ensures transparency, compliance, and accountability throughout the project financing process.

Through a comprehensive approach that involves multiple stakeholders, including sponsors, lenders, off-takers, and guarantors, projects are financed, implemented, and managed efficiently, contributing to the country’s sustainable economic progress.

As Bangladesh continues to prioritize its industrial and infrastructure development, industrial project finance will remain a key mechanism for mobilizing domestic and foreign investments.

The collaboration between the public and private sectors, underpinned by sound legal and regulatory principles, will shape Bangladesh’s economic landscape and lead the nation toward prosperity and development.

Additional securities such as sponsor support and guarantee:

In Bangladesh, project financing is primarily conducted on either a non-recourse or limited recourse basis. Non-recourse financings are typically secured by collateral, while limited recourse financing involves additional securities such as sponsor support and guarantees. The following sources of funding are typically available for projects in Bangladesh:

a. State-owned commercial banks:

Bangladesh has six state-owned banks that actively participate in project financing.

b. Specialized banks:

These state-owned banks focus on specific sectors and areas, contributing to project funding.

c. Private commercial banks:

There are 40 local licensed banks and nine licensed branches of foreign banks operating in Bangladesh, providing financing options for various projects.

e. Foreign multilaterals and development finance institutions:

These institutions are permitted to finance local projects.

f. Foreign banks/financial institutions:

Foreign entities are allowed to finance projects within Bangladesh.

g. Government funds:

The government provides funds to support Public-Private Partnership (PPP) projects facing short-term economic challenges, including Viability Gap Financing (VGF) and the Bangladesh Infrastructure Finance Fund (BIFF).

Major Types of Financings in Bangladesh:

Several types of financing are commonly adopted in local projects in Bangladesh, including:

a. Buyers’ credit:

Project infrastructure buyers can directly obtain loans from lenders to finance their purchases. b. Suppliers’ credit:

Suppliers either arrange a loan to finance their credit sales or extend credit to the buyers themselves, with agreed-upon mark-ups. c. Lease finance:

This option is widely used in the local market, wherein a leasing company leases equipment under financial or operational leases.

Cross-border lease finance is structured as a supplier credit. d. Islamic finance: Islamic financing is gaining popularity in Bangladesh, especially for acquiring high-cost equipment and machinery. Common arrangements include sale and leasebacks (Ijarah), musharaka leasing, one-step murabaha, two-step murabaha, and commodity murabaha.

Advantages and Disadvantages of Project Financing:

Project financing offers several advantages for sponsors and lenders:

Advantages:

a. Risk-sharing: Project financing enables sponsors to share project risks with other stakeholders through security arrangements and contractual agreements.

b. Cash flow management: Lenders can manage free cash flow after operational expenses and statutory payments, leading to a lower cost of capital compared to equity.

c. Lower cost of capital: In the long term, the cost of capital is generally lower compared to the cost of equity.

d. Limited liabilities: A special project vehicle helps sponsors limit their liabilities in project financing.

Disadvantages:

a. Complexity:

Project financing deals are complex due to the need to structure multiple contracts negotiated by all parties involved.

b. Higher transaction costs:

The complexity of project financing leads to higher transaction costs, including legal expenses, tax, and preparation of ownership and loan documentation.

Corporate Vehicles for Project Financing:

In Bangladesh, limited liability companies are typically used for project financing due to various reasons:

Limited liability companies are preferred by local entrepreneurs for their limited liability. c. Appropriate for non-recourse or limited-recourse financing.

Typical Documents in a Project Financing Transaction:

Several essential documents are involved in a project finance transaction in Bangladesh, including:

a. Termsheet:

A summary of the key terms and conditions of the financing arrangement.

b. Facility agreements: Agreements defining the terms of the financing provided by lenders.

c. Security agreements: Contracts outlining the forms of security granted to lenders.

d. Inter-creditor agreements: Agreements among multiple creditors defining their respective rights and priorities.

e. Account bank/escrow agreements: Agreements governing the use of accounts or escrows for fund management.

f. Cost over-run/sponsor support agreements: Agreements where sponsors pledge to support the project financially in case of cost overruns.

g. Guarantees: Agreements providing additional financial support and protection to lenders.

h. Direct agreements: Agreements between lenders and project parties, ensuring lenders’ direct access to project cash flows and collateral.

Forms of Security in Project Financing:

The main forms of security used in project financing in Bangladesh include:

a. Mortgages: Commonly used for immovable assets such as land and buildings.

b. Fixed and floating charges: Fixed charges grant control over assets, while floating charges allow the chargee to deal with charged assets until crystallization.

c. Pledge of shares: Shareholders can pledge company shares in favor of lenders.

d. Corporate guarantees: Shareholders and third parties can provide guarantees for loans.

e. Bank guarantees: Separate approval from the Bangladesh Bank is required for bank guarantees.

f. Liens: Strictly defined and governed by relevant statutes and conventions.

g. Assignment of receivables: Common for taking security over contractual rights.

Insurance Arrangements for Projects in Bangladesh:

Insurance is a crucial aspect of project financing in Bangladesh, providing protection against various risks that projects may encounter. Common insurance arrangements for projects in the country include:

b. Burglary, natural disaster, and fire insurance:

These insurances protect against losses caused by burglary, natural disasters, and fire incidents, providing additional security to project assets and infrastructure.

c. Third-party liability insurance:

Projects often carry third-party liability insurance to protect against claims from third parties in case of property damage, bodily injury, or other liabilities arising from the project’s activities.

d. Employer’s liability insurance:

This insurance covers liabilities arising from workplace-related injuries or accidents, ensuring protection for employees and laborers involved in the project.

Lenders’ Protection Concerning Project Insurance:

In project financing, lenders have a vested interest in ensuring adequate insurance coverage for the project’s various elements. To protect their interests regarding project insurance, lenders typically adopt the following measures:

a. Beneficiary of project insurance:

Lenders often nominate themselves as the principal beneficiary of the project insurance policies. This allows them to have direct access to insurance proceeds in case of any covered incidents.

b. Compliance monitoring:

Lenders may require borrowers to provide regular updates on insurance coverage and policy renewals to ensure continuous protection throughout the project’s duration.

c. Escrow arrangements:

In some cases, lenders may set up escrow accounts to hold insurance proceeds. This ensures that the funds are available for necessary project repairs or replacements in case of an insured event.

d. Verification of coverage:

Lenders may conduct periodic checks to ensure that the insurance policies meet the required coverage levels and address potential risks adequately.

e. Review of policy terms:

Lenders carefully assess insurance policies to ensure that the coverage aligns with the project’s specific risks and liabilities.

Mechanisms to Protect Security Interests:

Security interests must be perfected within the prescribed period with the relevant authorities. Subsequent interest acquirers are deemed to have notice of the security from the date of its perfection.

Subsequent mortgages or charges require approval from the prior chargee or mortgagee, but subordinated or pari-passu charges can be created with prior approval.

Public Private Partnerships (PPPs) in Bangladesh:

Until 2010, Bangladesh lacked a specific PPP framework. However, in 2010, the government introduced the Policy and Strategy for Public-Private Partnership to promote private sector participation in infrastructure development. This move aimed to address the challenges of funding and executing large-scale projects while leveraging private sector expertise and efficiency.

To support the PPP process and infrastructure development in Bangladesh, the government enacted several regulations and guidelines:

Procurement Guideline for PPP Projects 2016:

The Procurement Guideline provides a framework for transparent and competitive procurement processes for PPP projects. It ensures that project contracts are awarded through fair and open procedures, promoting accountability and reducing the risk of corruption.

Guidelines for Unsolicited Proposals 2016:

The Guidelines for Unsolicited Proposals allow private sector entities to submit project proposals to the government for consideration. These proposals are evaluated based on their feasibility, economic and social benefits, and alignment with national development priorities. Successful proposals may lead to PPP project development.

Guideline for Viability Gap Financing for PPP Projects 2012:

The Guideline for Viability Gap Financing outlines the mechanism through which the government provides financial support to PPP projects that have high economic and social viability but lack complete financial viability. Viability Gap Financing can be in the form of a capital grant or annuity payment.

Guideline for PPP Technical Assistance Financing 2012 & Scheme for PPP Technical Assistance Financing 2012:

The government offers technical assistance financing to support the preparation and development of PPP projects. These guidelines and schemes aim to strengthen project preparation and enhance the overall viability of projects.

PPP Screening Manual:

The PPP Screening Manual provides guidance on project screening and selection criteria for potential PPP projects. This process helps prioritize projects with significant development impact and ensures that viable projects receive attention.

Financing PPP Projects in Bangladesh:

PPPs in Bangladesh are typically financed through a combination of funding sources, including multilateral institutions, development finance institutions, and private commercial banks. While the government may not provide payment guarantees for PPP projects, it does play a role in supporting financing through various mechanisms:

Viability Gap Financing (VGF):

As mentioned earlier, VGF is provided to projects with high economic and social viability but uncertain financial viability. The government’s financial support enhances the feasibility of these projects and encourages private sector participation.

Infrastructure Financing:

Specialized financial institutions like the Bangladesh Infrastructure Finance Fund (BIFF) and Infrastructure Development Company Limited (IDCOL) provide financing facilities for PPP projects in the form of debt or equity. The government may participate in such financing arrangements through budget provisions.

Financing against Linked Components:

The government may consider financing and implementing linked activities, such as land acquisition, rehabilitation, provision of utility services, and construction of approach roads. These complementary activities contribute to the overall success of the main PPP project.

Security and Guarantees in PPP Projects:

In PPP projects, concessionaires (private entities) may be allowed to give security to lenders over their interests in the project company, subject to approval from the grantor (government). This security allows lenders to have recourse to the assets of the project company in case of default, providing them with an additional layer of protection.

Social, Ethical, and Environmental Issues:

Social and ethical issues play a significant role in project financing in Bangladesh. The country has ratified the UN Convention against Corruption and has enacted specific laws to address corrupt practices, money laundering, and human rights abuses. Fair practices across all spheres of social, economic, and political activities are ensured through various laws, including the Prevention of Corruption Act, Money Laundering Prevention Act, and Right to Information Act.

Additionally, environmental concerns are addressed through adherence to the Environmental Policy and Bangladesh Environment Conservation Act. Compliance with international guidelines like the IFC Performance Standards and Equator Principles is also required to meet environmental and social requirements.

Tax Holidays and Incentives for Foreign Investment in Projects:

Foreign investment plays a crucial role in the development of infrastructure projects in Bangladesh. To attract foreign investors, the government offers various tax holidays and incentives. Let’s explore some of these incentives and how they encourage foreign investment in the country:

Tax Holidays for Thrust Sectors and Infrastructure Projects:

The government provides tax holidays for industrial undertakings and physical infrastructure facilities established in thrust sectors. Thrust sectors refer to industries that have significantly contributed to the country’s industrialization. Additionally, industries set up in Export Processing Zones (EPZs) are also eligible for tax holidays. The duration and extent of the tax holidays vary based on the location of the project and the type of industry.

Accelerated Depreciation:

Industrial undertakings not benefiting from tax holidays can take advantage of accelerated depreciation allowances. This allows them to claim higher depreciation in the early years of the project, reducing their taxable income and, consequently, their tax liability.

Concessionary Duty on Imported Capital Machinery:

Industries with an annual turnover below a certain threshold may benefit from a concessionary import duty rate of 3% on capital machinery and spares. This measure reduces the cost of setting up the project and enhances the attractiveness of foreign investment.

Incentives for Export-Oriented Industries:

Export-oriented industries enjoy a range of incentives to boost their competitiveness in the global market. These incentives include duty-free import of capital machinery and spares, bonded warehousing, access to loans and funds for export promotion, cash incentives and export subsidies, and more.

Double Tax Avoidance Agreements (DTAs) and Bilateral Investment Treaties (BITs):

Bangladesh has entered into DTAs with several countries and BITs with various other nations to avoid double taxation of income and protect foreign investments. These agreements provide certainty and predictability to foreign investors, assuring them of fair treatment and non-discrimination.

Power and Energy Fast Supply Enhancement (Special Provision) Act 2010 (PEFSE):

The PEFSE Act empowers the government to quickly deal with and accept solicited or unsolicited proposals in the power and energy sectors on an emergency basis. It allows the government to enter into arrangements with companies bypassing the usual procurement processes. Moreover, it indemnifies the government against any legal proceedings relating to the award of contracts under the PEFSE.

Foreign Currency Accounts:

While opening and operating onshore and offshore foreign currency accounts are generally prohibited without approval from the Bangladesh Bank, there are exceptions for specific projects. For instance, under the private power generation policy, private power generation companies have been granted the right to open and maintain onshore foreign currency accounts.

Dividend Repatriation and Shareholder Loans:

There are no restrictions on the payment of dividends or repayment of shareholder loans to a foreign parent company. However, for the repayment of shareholder loans, prior approval from the Bangladesh Bank is required.

Choice of Law and Jurisdiction

Foreign Law: When parties enter into a project contract or financing agreement, they have the option to choose foreign law as the governing law for the contract. The Bangladesh courts will uphold such a choice of foreign law, provided the intention to do so is clearly expressed in the contract. This decision was reinforced by the precedent set in PLD 1964 Dacca 637, which establishes that the expressed intention of the contractual parties regarding the law governing the contract overrides any other presumption.

Jurisdiction: If a project contract or financing agreement designates a foreign court as having exclusive or non-exclusive jurisdiction, the Bangladesh courts will respect this choice. In such cases, the Bangladesh courts will not exercise jurisdiction over contractual disputes unless all parties involved in the dispute agree to submit to the jurisdiction of the Bangladesh courts. However, it’s worth noting that the Bangladesh courts may assume jurisdiction in specific cases where they have exclusive jurisdiction, such as labor disputes.

Enforceability of Waivers of Immunity

In the context of international contracts that do not contravene local policy and are otherwise valid and binding, Bangladesh courts recognize waivers of sovereign immunity. Additionally, for disputes arising out of commercial contracts, the Bangladesh courts accept the common law doctrine of restrictive immunity, which has been adopted by the English courts.

Recognition of Foreign Arbitral Awards and Court Judgments

Foreign Money Judgment: Under the Code of Civil Procedure 1908, a foreign money judgment can be enforced in Bangladesh within six years from the date of the judgment, subject to court approval for longer durations. To be enforceable, the foreign judgment must fulfill several requirements, including being conclusive and given on the merits of the case, pronounced by a court of competent jurisdiction, and capable of enforcement in the original court.

It must not have been obtained through fraud, be contrary to public policy or applicable laws of Bangladesh, or sustain a claim based on a breach of a law in force in Bangladesh. Furthermore, there should be no pending or possible appeal against the judgment in the original court.

Foreign Arbitral Award: The recognition and enforcement of foreign arbitral awards are subject to certain grounds in Bangladesh. The courts may decline to enforce a foreign arbitral award if a party to the arbitration agreement was under some incapacity, if the arbitration agreement is not valid under the agreed law, or if the party against whom the award is invoked was not given proper notice or an opportunity to present their case.

The award may also be denied enforcement if it contains decisions on matters beyond the scope of the submission to arbitration, except for the part related to the submitted matters. Moreover, the composition of the arbitral tribunal or the arbitral procedure should be in accordance with the parties’ agreement and the law of the country where the arbitration took place.

Enforcement can also be denied if the award is not yet binding on the parties, has been set aside or suspended by the competent authority in the country where it was made, or if the subject matter of the dispute is not capable of settlement by arbitration under the law of Bangladesh, or if the recognition and enforcement would be contrary to public policy.

Recent Legal Developments in Project Finance

As of now, there are no current proposed legal reforms impacting project finance in Bangladesh. However, the landscape of local project financing has seen a new addition in the form of Export Credit Agency (ECA) backed finances. The Bangladesh Investment Development Authority evaluates projects based on its prior payment requirements for the ECA premium, leading to two primary disbursement methods: direct disbursement and reimbursement.

Hire the best law firm for Project finance in Bangladesh

Navigating international projects and finance in Bangladesh requires a keen understanding of the country’s legal framework. Parties can choose foreign law as the governing law for contracts, and the courts respect such choices.

Additionally, waivers of immunity are enforceable in specific circumstances, and the recognition of foreign arbitral awards and court judgments follows set criteria. Staying up-to-date with legal developments is essential, particularly in project finance, where ECA-backed finances are becoming an important consideration. As Bangladesh continues to engage in global business ventures, consulting with legal experts is vital to ensure compliance and successful outcomes in cross-border transactions.

Tahmidur Rahman Remura Wahid Associates represents a variety of high-profile clients operating in Bangladesh to carry out specific projects such as power plants, roads and motorways, and so on. They frequently require financing from many financial institutions, and our lawyers assist clients in creating the relevant documentation as well as advising them on any legal difficulties that may develop as a result of such transactions. Tahmidur Rahman Remura Wahid Associates Associates also aids clients by supplying them with lawyers who negotiate with financial institutions on their behalf.

GLOBAL OFFICES: DHAKA: House 410, ROAD 29, Mohakhali DOHS DUBAI: Rolex Building, L-12 Sheikh Zayed Road LONDON: 1156, St Giles Avenue, 330 High Holborn, London, WC1V 7QH

External Commercial Borrowing (ECB) is the borrowing of funds from international lenders by a country’s business sector. In Bangladesh, the ability of private firms to access foreign currency loans from outside financial institutions or corporations has aided industrial growth, particularly in the context of new projects, expansion, and capital goods imports.

The architecture and effectiveness of foreign commercial borrowing in Bangladesh are examined in this essay, with an emphasis on private sector external debt. It examines the approval procedure, the sorts of projects sponsored, and the economic consequences of such borrowing.

The Eligibility and Approval Process

Private enterprises registered with the Board of Investment (BOI) and incorporated under the Companies Act of 1994 are eligible to apply for external commercial financing. These borrowers can look to organizations or individuals in other countries for commercial loans, financial loans, bank loans, buyer’s credit, or supplier’s credit. However, it is vital to highlight that foreign loans cannot be utilized for working capital or capital market investment.

Companies must receive approval from the Scrutiny Committee of the Board of Investment, which is chaired by the Governor of the Bangladesh Bank (BB), in order to acquire foreign loans.

The application process requires the submission of the required documents, which include the Certificate of Incorporation, Memorandum and Articles of Association, Term-sheet or Loan Agreement, feasibility report, financial analysis, equity forms, and other appropriate credentials. The Scrutiny Committee assesses these applications based on business viability, borrower creditworthiness, repayment length, and debt-equity ratio, among other factors.

Foreign-owned (100%) investment projects in Export Processing Zones (EPZ) are exempt from obtaining prior clearance from BIDA or BB for foreign currency loans from overseas financial institutions or corporations.

The Power Sector and Other Requirements

The Power Sector has unique requirements for external commercial borrowing in addition to the standard requirements. For this sector, the Letter of Intent, Implementation Agreement, and Power Purchase Agreement are required papers.

External Borrowing Trends in the Private Sector

An examination of private sector external borrowing in Bangladesh from 2011 to 2013 indicated a considerable increase in sanctioned loans. In 2011, about 20 private firms were approved for loans totaling USD 936.30 million. In 2012, this value climbed to USD 1579.57 million among 81 firms, while in 2013, it increased to USD 1555.33 million among 116 enterprises. During this time, around 55 enterprises gained clearance for loans worth USD 1357.06 million on an annual basis.

However, in comparison to the permitted loans, the disbursement of external debt was comparatively modest, creating concerns that require additional study.

Debt Sustainability Analysis

In November 2013, the International Monetary Fund (IMF) and the International Development Association (IDA) conducted a Debt Sustainability Analysis (DSA), which found that Bangladesh was unlikely to encounter severe debt-related stress in the next two decades. The DSA took into account both domestic and external debt numbers and predicted various debt indicators up to 2034 under various scenarios.

The DSA results demonstrated Bangladesh’s resilience to debt-related shocks, particularly external debt, making a solid case for permitting additional private external loans into the economy.

A survey of thirteen private enterprises from various industries, including RMG, footwear, telecommunications, power generation, and pharmaceuticals, revealed information about the effectiveness of external commercial borrowing in Bangladesh. Between 2007 and 2013, these corporations borrowed a total of USD 894.24 million.

According to the poll, the key reasons for borrowing from foreign sources were lower interest rates compared to domestic possibilities and the inability of local banks to provide large financing due to insufficient capital bases. The majority of the borrowed funds were used to import capital machinery for new projects or expansion of existing ones, demonstrating that the loans were put to good use.

External commercial borrowing has been critical in propelling Bangladesh’s industrial growth and development. Foreign currency loans have helped private sector businesses fund new initiatives and grow existing operations. BIDA and the Scrutiny Committee manage the clearance procedure, which guarantees that the borrowing is consistent with the country’s economic priorities and financial stability.

Despite the efficiency of external commercial borrowing, the low proportion of disbursements relative to approved loans warrants more investigation. The Debt Sustainability Analysis, on the other hand, reassures that Bangladesh is well-equipped to deal with debt-related difficulties, particularly external debt concerns.

External commercial borrowing has aided Bangladesh’s economic development by providing private firms with critical resources for growth and development. As long as the borrowing is consistent with the country’s economic goals and regulatory safeguards are in place, it can serve as a catalyst for long-term development and prosperity.

External Commercial Borrowing (ECB) in Bangladesh

Question

Answer

What is External Commercial Borrowing (ECB)?

External Commercial Borrowing (ECB) refers to the borrowing of funds by private sector enterprises in Bangladesh from foreign lenders in foreign currency.

It includes commercial loans, buyer’s and supplier’s credit, etc., primarily used for importing capital goods, financing new projects, or expanding existing production facilities.

Which entities are eligible for ECB in Bangladesh?

Private enterprises incorporated under the Companies Act 1994 and registered with the Board of Investment (BOI) are eligible to apply for External Commercial Borrowing (ECB) in Bangladesh.

What are the main purposes for obtaining ECB?

The main purposes for obtaining ECB in Bangladesh include financing new projects, importing capital machinery, and expanding existing production facilities. It is not permitted to use foreign loans for working capital purposes or investment in the capital market.

What is the role of Bangladesh Investment Development Authority (BIDA)?

BIDA plays a vital role in the ECB process. It scrutinizes and approves applications for foreign loans, ensuring that they align with the country’s economic priorities and financial stability. The applications are then submitted to the Scrutiny Committee headed by the Governor of Bangladesh Bank (BB) for final approval.

Are foreign-owned investment projects exempt from approval?

Yes, foreign-owned (100%) investment projects located in Export Processing Zones (EPZ) may obtain foreign currency loans from overseas financial institutions or entities without prior approval from BIDA or BB.

What documents are required for ECB approval?

The application for ECB approval must be submitted with several supporting documents:

including the Certificate of Incorporation, Memorandum and Articles of Association of the company, Term-sheet or Loan Agreement with repayment details, financial analysis, board resolution related to the proposed borrowing, feasibility report of the investment project, relevant equity forms, bank certificate on creditworthiness, and track record of foreign borrowing.

Additional documents may be required for specific sectors like the Power Sector.

How are ECB applications processed?

After submission, ECB applications are duly scrutinized by BIDA. Upon satisfactory evaluation, they are forwarded to the Scrutiny Committee, which includes the Governor of Bangladesh Bank (BB), for final approval. The process has been streamlined through BIDA’s online OSS platform.

What is the trend of private sector external borrowing in Bangladesh?

The trend of private sector external borrowing in Bangladesh has shown significant growth in approved loans over the years. Between 2011 and 2013, around 81 enterprises were approved for loans totaling USD 1579.57 million, increasing from USD 936.30 million among 20 enterprises in 2011.

However, there has been a relatively low proportion of disbursement compared to approved loans, warranting further investigation.

What does the Debt Sustainability Analysis (DSA) indicate?

The Debt Sustainability Analysis (DSA) jointly conducted by the International Monetary Fund (IMF) and the International Development Association (IDA) suggests that Bangladesh is highly unlikely to face significant debt-related stress within the next two decades.

The analysis considers both domestic and external debt and projects various debt indicators up to 2034, demonstrating the nation’s resilience to shocks related to debt conditions, particularly external debt.

How have private companies used external loans?

A survey of selected private companies between 2007 and 2013 revealed that the borrowed funds were primarily used for importing capital machinery to expand existing projects or establish new ones.

The loans were found to be utilized productively, with most companies benefiting from lower interest rates and the availability of substantial financing for their projects.

Company Law practice in TRW law firm in Bangladesh

The Barristers, Advocates, and lawyers at TRW Law chamber in Mohakhali DOHS, Dhaka, Bangladesh are highly experienced at assisting clients in dealing with and registering branch offices in Bangladesh. For queries or legal assistance to set up a branch office in Bangladesh, please reach us at:

E-mail: info@trfirm.com Phone: +8801847220062 or +8801779127165 or +8801708080817 House 410 Road 29 Mohakhali DOHS

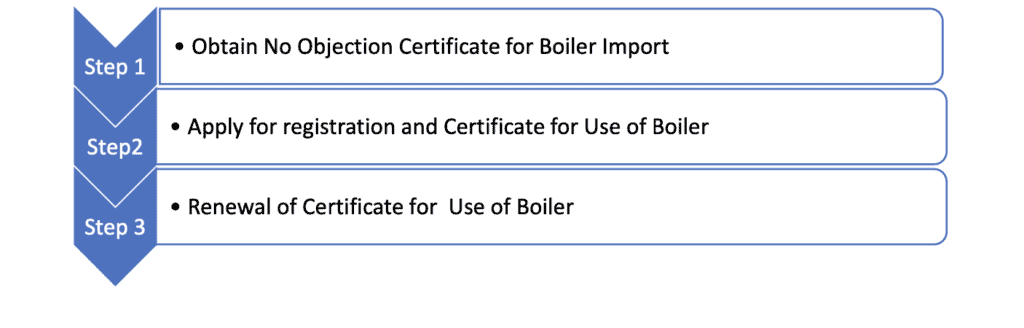

Boiler Registration Certificate for BEZA in Bangladesh

In order to install and use a boiler with a volumetric capacity greater than 25 liters for their manufacturing or production unit, an EZ Unit Investor must first obtain a No Objection Certificate (NOC) from the Office of the Chief Inspector of Boilers (OCIB) through BEZA-OSS Center for importing the boiler, which is housed within the Ministry of Industry of the Government of Bangladesh, and a boiler license (which is renewable annually).

The Boiler Certificate must be renewed annually in accordance with the EZ Unit Investor’s application and certain assessment procedures. The following flowchart depicts these processes in sequential order:

Step 01: NOC for Boiler Import –

Documents Required:

Electronic Application Form submitted online

Cross-Sectional Construction Drawing Approved by the Recognized/Competent/Inspecting Authority

Heating Surface Calculation for the Boiler (Photocopy)

Calculation of Pressure Boiler Parts’ Strength (Photocopy)

Steel Manufacturer’s Certificate of Origin and Test Results (Photocopy)

Pro-forma Invoice (Photocopy, if boiler is imported)

Trade License (Photocopy)

Payment evidence/Application fee

Process:

Listed below are the Procedures for Obtaining a No Objection Certificate (NOC):

The Applicant visits the BEZA-OSS website, completes the online application form, and submits it alongside the previously listed required documents.

The BEZA-OSS Center evaluates the submitted documents.

The BEZA-OSS Center transmits the documents to the OCIB

The OCIB then issues a NOC and transmits it to the BEZA OSS.

BEZA OSS Center will issue the NOC to the Applicant.

Timeframe: three days (anticipated).

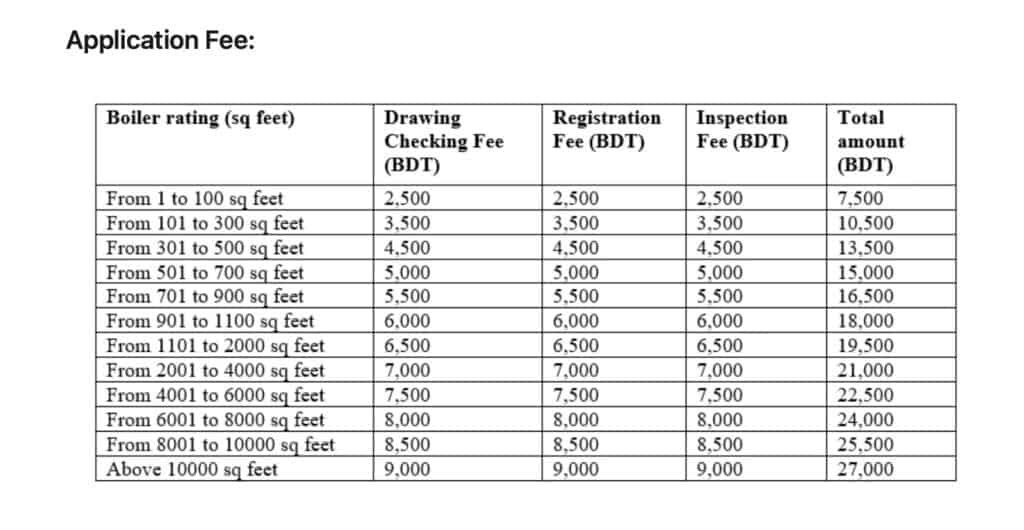

Application Fee: The application Fee varies based on the thermal surface/rating of the imported Boiler.

Note: VAT will be levied when payments are made.

Step 02: Boiler Registration

Documents Required:

Electronic Application Form submitted online

Cross-Sectional Construction Drawing with Scale that has been authorized by the competent authority

Heating Surface of the Boiler Calculation

Calculation of Pressure Parts of the Boiler’s Strength

Certificate of Inspection Authority During Manufacturing (Original)

Certificate of Manufacture and Test Results from the Boiler Manufacturer (Original)

Steel Manufacturer’s Certificate of Origin and Test Results (Photocopy)

Steel Manufacturer’s Certificate for Steam Pipe with a Diameter Greater Than 3 Inches (Photocopy)

Manufacturer’s mark (Copy)

Credit Letter (Photocopy)

Bill of Lading (Reproduction)

Certificate of Boiler Attendant (Photocopy)

Process:

The Applicant visits the BEZA-OSS website and completes the online application form with the required boiler registration documents and drawings.

The BEZA OSS Center transmits the application and supporting documentation to the OCIB.

OCIB designates an Inspector who will schedule the inspection date.

The BEZA-OSS Center notifies the Applicant of the inspection date, procedure, and Inspector’s name, along with the inspection items.

On the predetermined date, the Inspector(s) conducts an inspection at the project site and observes various tests.

The Inspector prepares and finalizes the Inspection Report and makes recommendations to the Chief Inspector of Boilers.

If the boiler inspection report is satisfactory, the Chief Inspector of Boilers issues a letter verifying the boiler’s registration along with the boiler’s Certificate for Use.

The OCIB dispatches the Boiler Registration Letter and Certificate to the BEZA OSS Center for use of the boiler.

The BEZA OSS Center then provides the Applicant with both the Boiler Registration Letter and the Certificate.

Timeline:

15 working days (based on the required inspection frequency and distance for furnaces of varying sizes).

Note: The Applicant must employ the required number of certified Boiler Attendants as full-time employees to operate and maintain the Boiler.

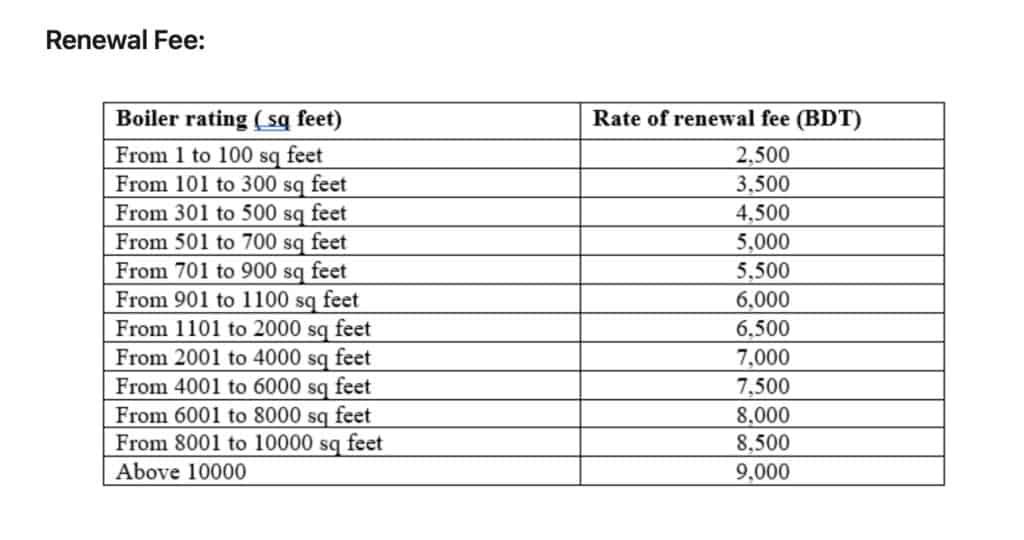

Step 3: Boiler Certificate Renewal

Documents Required:

Electronic Application Form

evidence of payment of the renewal fee

Certificate of Boiler Operator

Process:

The Applicant visits the BEZA-OSS website at least 30 days prior to the expiration of the Boiler Certificate and completes the online application form.

The BEZA OSS Center then transmits the application and supporting documents to the respective inspector/OCIB, who will schedule an inspection date.

The BEZA-OSS Center notifies the Applicant of the inspection date and inspector’s name within three days of receiving the application.

The Inspector performs an inspection at the construction site.

The Inspector is responsible for preparing the Inspection Report.

In the event that the Inspector makes any comment, observation, or instruction regarding the improvement of construction works, the Applicant takes appropriate action and submits the implementation report along with photographs to the BEZA-OSS Center, which then sends the report to the OCIB.